Nurphoto | Nurphoto | Getty Images

As mortgage rates reached a 23-year high last week, the cry went off across markets and social media: Is housing affordability dead? Has a version of the American dream — home ownership, kids, backyard barbecues — died with it?

The question is sharp because housing affordability has dropped by nearly half since the ultra-low interest rate days of 2021, according to the National Association of Realtors.

The median family was already $9,000 short in August of the income needed to buy the median existing home, the association says, and the recent surge in rates since has moved another five million U.S. families below the qualification standard for a $400,000 loan, according to John Burns Real Estate Consulting. At 3% mortgage rates, 50 million households could get a loan that size. Now it’s 22 million.

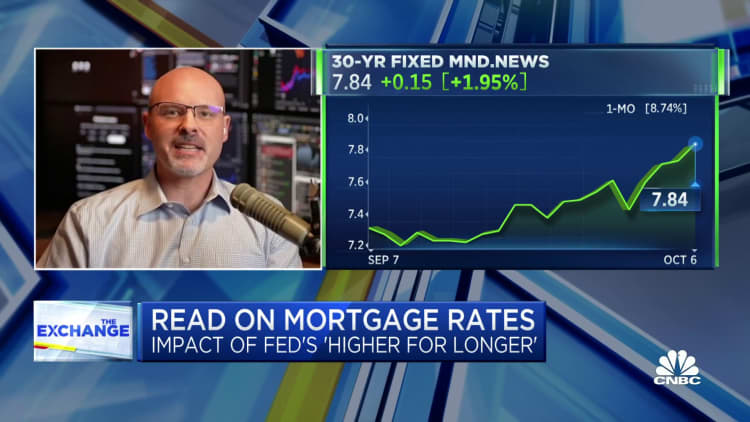

While an easing in treasury bond yields this week has brought the 30-year fixed mortgage back a shade below 8%, there is no quick fix.

The qualifying yearly income for a median-priced house in 2020 was $49,680. Now it’s more than $107,000, according to the NAR. Redfin puts the figure at $114,627.

“[These are] stunning numbers that render house affordability even more challenging for too many American families, especially those looking to buy their first home,” bond-market maven Mohamed El-Erian, an advisor to Allianz among many other roles, posted on X.

“It’s a very worrisome development for America,” NAR chief economist Lawrence Yun said.

Affordability depends on three big numbers, according to Yun — family income, the price of the house, and the mortgage rate. With incomes rising since 2019, the bigger issue is interest rates. When they were low, they papered over a surge in housing prices that began in late 2020, helped by people relocating to areas like Florida, Austin, Texas, and Boise, Idaho, to work in their old cities from their new homes. Now, the surge in rates is crushing affordability even as incomes rise sharply and housing prices mostly hang on to the big gains they generated during Covid.

“At the current 8% mortgage rate, mortgage payment[s] are 38% of median income,” Moody’s Analytics chief economist Mark Zandi said. “The mortgage rate has to fall to 5.5%, or the median priced home has to fall by 22%, or the median income has to increase by 28%, or some combination of all three variables.”

At the same time, demand for adjustable-rate mortgages has spiked to its highest level in a year amid the broader slowdown in mortgage applications.

What needs to change to make housing affordable again

All three indicators face a tough road back to “normal,” and normal is a long way from here. A few numbers illustrate why.

The National Association of Realtors measures affordability through its 34-year old Housing Affordability Index, or HAI. It calculates how much income the median family has to have to afford the median existing home, which, right now, costs about $413,000, according to NAR. If the index equals 100, it means the median family has enough income to buy that house with a 20% down payment. The index assumes the family wants to pay 25% of its income toward principal and interest.

The long-term average of the HAI is 138.1, meaning that, normally, the median family has a 38% cushion. Its all-time high was 213 in 2013, after the housing bust and 2008 financial crisis.

Right now, that index stands at 88.7.

A few scenarios using NAR data help illustrate how far affordability is from the average between 1989 and 2019, and what would be required to push it back into a more typical range as the national average for the 30-year ticked lower to 7.98% on Tuesday.

- If home prices are stable, rates need to fall to 3.55% in order to be back to historical average.

- If prices grow 5%, rates need to fall to 3.16%.

- If prices stay the same but incomes increase 5%, rates need to fall to 3.95%

- A mortgage rate that stays around 8% means median home prices need to fall by 35%, to $265,000.

- If rates stay at 8% and prices at current levels, income needs to increase by 63%.

But these numbers understate the challenge of getting affordability back to where Americans are used to seeing it.

Getting back to the affordability people enjoyed during the hyper-low interest rates of the pandemic would take even more: The HAI reached a yearly average of 169.9 that year, a level few think will come back any time soon.

Affordability became stretched partly because home prices rose 38% since 2020, according to the NAR, but more important was the jump in average interest rates from 3% in 2021 to as high as 8% last week. That’s a 167% jump, driving a $1,199 increase in monthly payments on a newly bought house, per NAR.

Higher wages are a plus, but not enough

Rising incomes will help, and median family incomes have climbed 16% to more than $98,000 since 2020. But that isn’t nearly enough to cover the affordability gap without devoting a higher share of the household paychecks to the mortgage, said Zandi.

Aside from the raw numbers, the direction of monetary policy will keep incomes from fixing the housing problem, said Doug Duncan, chief economist at Fannie Mae. The Federal Reserve has been raising interest rates precisely because it thinks wages have been growing fast enough to reinforce post-Covid inflation, Duncan said. Year-over-year wage gains slipped to 3.4% in the most recent job-market data, he said, and the Fed would like wage growth to be lower.

Downward pressure on home prices would help, but it does not look like they will decline by much. And even if home prices do the decline, that trend won’t be sustainable unless America builds millions of more homes.

After prices surged from 2019 through early 2022, it was easy to assume a big price correction coming, but it hasn’t happened. In most markets, prices have even begun to turn up a little bit. According to the realtors’ association, the median price of an existing home dropped by more than $35,000 in late 2022 but has risen by $45,000 since its low in January.

Not enough new housing in America

The biggest reason is that so few homes are up for sale that the laws of supply and demand aren’t working normally. Even with demand hit by affordability woes, buyers who are out there have to compete for so few homes that prices have stayed close to balanced.

“Boomers are doing what they said they were going to do. They are aging in place,” Duncan said. “And Gen X is locked into 3% mortgages already. So it’s up to the builders.”

The builders are kind of a problem, said Redfin chief economist Daryl Fairweather. They’ve been boosting profits this year, and BlackRock’s exchange traded fund tracking the industry is up 41%, but Fairweather said they’ve barely begun to address a long-term housing shortage Freddie Mac estimated at 3.8 million homes before the pandemic, a number that has likely grown since.

Builders have begun work on only 692,000 new single-family homes this year, and 1.1 million including condominiums and apartments, she said. So it will take nearly four years to build enough houses to rebuild supply, and that leaves out new household formation, she added. Meanwhile, apartment construction has already begun to slow, and builders are pulling back on mortgage buydowns and other tactics they have used to prop up demand.

There are reasons to believe more buyers could materialize. Duncan said the millennial generation is just moving into peak home buying years now, promising to add millions of potential buyers to the market, with the biggest annual birth cohorts reaching the average first-time purchase age of 36 years around 2026. If rates do begin to decline, Fairweather predicts that will bring more buyers back into the market, but inevitably push prices back up toward previous peaks, which there had been signs of earlier this year when mortgage rates dipped to 6% in early March.

“We need a couple of years more building at this pace, and we can’t sustain the demand because of high interest rates,” Fairweather said.

The Fed and the bond market are big problems

There are two problems with mortgage rates right now, economists say. One is a Fed that is determined to not declare victory over inflation prematurely, and the other is a hypersensitive bond market that sees inflation everywhere it looks, even as the rate of price increases throughout the economy has dropped markedly.

Mortgage rates are 2 percentage points higher than in early March – even though trailing 12-month inflation, which higher interest rates theoretically hedge against, has dropped to as low as 3.1% from 6% in February. That’s still above the Fed’s 2% target for core inflation, but a measure of inflation excluding shelter costs — which the government says are up 7% in the last year despite declines or much smaller gains in housing prices reported by private sources — has been 2.1% or lower since May.

The Fed has only raised the federal funds rate by three-fourths of a point since then, as part of its “higher for longer” strategy — maintaining higher interest rates rather than aggressively adding more rate hikes from here. The biggest reason mortgages have surged of late is the bond market, which pushed 10-year Treasury yields up by as much as 47%, for a full 1.6 percentage points. On top of that, the traditional spread between 10-year treasuries and mortgages has widened to more than 3 percentage points — 1.5 to 2 points is the traditional range.

“It’s hard to justify the runup in rates, so it might just be volatility,” Fairweather said.

Even so, few economists or traders expect the Fed to push rates lower to help housing. The CME FedWatch tool, which is based on futures prices, predicts even if the central bank is done, or at least near done with its rate hikes, it won’t begin to cut rates until next March or May, and only modestly then. And spreads will likely remain extra-wide until short-term interest rates drop below the rates on longer-term treasuries, Duncan said.

It could take until 2026 to see a ‘normal’ real estate market

To get affordability back to a comfortable range will take a combination of higher wages, lower interest rates and stable prices, economists say, and that combination may take until 2026 or later to coalesce.

“The market is in a deep, deep freeze,” Zandi said. “The only way to thaw it out is a combination of lower prices, higher incomes and lower rates.”

In some parts of the country, it will be even harder, according to NAR. Affordability is even more broken in markets like New York and California than it is nationally, and moderate-income markets like Phoenix and Tampa are as unaffordable now as parts of California were earlier this year.

Until conditions normalize, the market will be the domain of small groups of people. Cash buyers will have an even bigger edge than normally. And, Yun says, if a buyer is willing to move to the Midwest, the best deals in the country can be found in places like Louisville, Indianapolis and Chicago, where relatively small rate cuts would push affordability near long-term national norms. Meanwhile, it’s going to be a slog across the nation.

“Mortgage rates will not go back to 3% – we’ll be lucky if we get back to 5,” Yun said.