10’000 Hours | Digitalvision | Getty Images

There’s still time to lower your 2023 tax bill or boost your refund with a lesser-known retirement savings strategy for married couples.

One requirement for individual retirement account contributions is “earned income,” such as wages or salary from a job or self-employment earnings. But there’s an exception for single-income households: the spousal IRA.

A spousal IRA is a separate Roth or traditional IRA for the non-working spouse — and it’s “often overlooked,” according to certified financial planner Judy Brown at SC&H Group in the Washington, D.C., and Baltimore area.

These accounts can provide a current-year tax break and boost retirement savings for nonearning spouses. As of 2021, some 18% of parents didn’t work outside of the home and most stay-at-home parents were women, according to Pew Research Center.

“My advice to [nonearning] women would be make sure you’re at least doing that spousal IRA,” said Boston-based CFP Catherine Valega, founder of Green Bee Advisory.

My advice to [nonearning] women would be make sure you’re at least doing that spousal IRA.

Catherine Valega

Founder of Green Bee Advisory

How the spousal IRA works

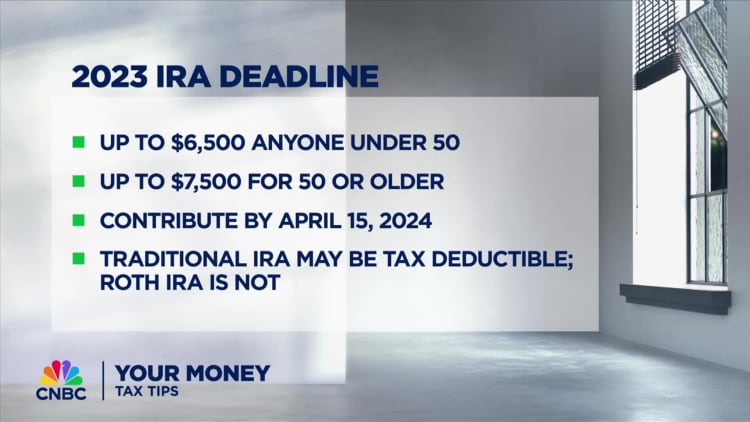

Married couples who file jointly have until the federal tax deadline — April 15 for most taxpayers — to make 2023 IRA contributions for each spouse, assuming there’s enough earned income for the combined deposits.

Traditional pretax spousal IRA contributions can provide a 2023 tax break, depending on income and workplace retirement plan participation, explained Brown, who is also a certified public accountant.

With income phaseouts for IRA deductibility and Roth IRA contributions, many wait until March or April for the previous year’s IRA deposits. It can be a “game-time decision” while doing your taxes, Brown said.

The annual IRA contribution limit is $6,500 for 2023 or $7,500 for savers age 50 and older. The limit increased to $7,000 for 2024, with an extra $1,000 for investors age 50 and up.

However, “it doesn’t have to be all or nothing,” Brown said. Even a $500 or $1,000 spousal IRA contribution could provide tax savings.

Contributions could create a ‘tax problem’

While spousal IRA contributions make sense for some couples, there are other factors to consider before making deposits, said CFP Laura Mattia, CEO of Atlas Fiduciary Financial in Sarasota, Florida.

For example, some couples need the extra cash for living expenses or shorter-term goals, like paying for a wedding, she said.

Plus, too much pretax retirement savings could create a “tax problem” in the future, depending on the size of your accounts and future required minimum distributions, Mattia said. Pretax withdrawals boost income, which can affect Medicare Part B and Part D premiums, among other consequences.

“It’s a puzzle and really depends on a lot of things,” she added.