Gilbert Michaud, a professor of environmental policy at Loyola University Chicago, said it’s worth looking into available options for solar right now.

Can solar panels save you money?

Interested in understanding the impact solar can have on your home? Enter some basic information below, and we’ll instantly provide a free estimate of your energy savings.

“It makes a lot of sense financially because costs have gone down so much and the incentives are really strong,” Michaud said.

Residential solar is very much a custom-fit product, however. To determine how much you can save, it’s important to be sure you consider all the factors influencing your unique situation.

Long-term solar savings

For most people, installing solar is an investment in the medium- to long-term future.

A payback period is the amount of time it takes to earn back your initial investment through monthly energy savings. How much you save per month depends on the size of your solar system, your home’s energy consumption and other factors.

Considering Solar Panels?

Our email course will walk you through how to go solar

Typically, excess solar energy produced by a residential system is credited against the amount used, but it’s rare to actually receive cash payments for solar power. Still, paying little or nothing to your local utility adds up to lots of savings over years or decades.

“Most systems pay themselves off in about 10 years. Then you have decades of free electricity after that,” explained Michaud.

Considering Solar Panels?

Our email course will walk you through how to go solar

He notes that some younger homeowners who move around more frequently might shy away from solar due to the perceived long commitment, but he points out that the investment can often be recouped from the increase in a home’s value that comes with a new installation.

The payback period will be unique to your circumstances because of the difference in both upfront solar costs and energy costs based on your location. But here are some guidelines to help you estimate when you’ll break even.

After solar panels save enough to pay for themselves, the rest is strictly savings.

Getty Images

How to estimate your solar savings

There’s a simple basic formula to determine how long it’ll take for your solar savings to pay off the cost of installing the system. Start with the upfront cost of installation, then subtract all tax credits, rebates, grants and other incentives you received. This determines your net system cost. Next, estimate how much you’ll save on your annual electricity bills with the system.

With a purchase as big as rooftop solar panels, you should get multiple quotes, make sure your solar installer answers all your questions, and find the offer that best fits your needs.

Subtract tax credits (and other incentives)

While tax credits and incentives vary state to state and utility to utility, the 30% federal solar tax credit applies to everyone. Find out how much you can expect your solar costs to be reduced, and subtract.

Watch this: Easy Ways to Lower Your Utility Bills and Save Money

Check your monthly electric bill savings

You could assume you’ll get all your power from solar, but while some homes will be able to zero out their electric bill, others will still have to pay for some electricity usage or standard fees. Some utilities charge fees just for staying connected to the grid. Savings will vary widely from home to home, depending on how many solar panels are installed, normal energy consumption and more.

Look at your electric bill — at least six months worth to account for seasonal temperature changes and other fluctuations in cost — and estimate your monthly savings from solar. If you cover 100% of your bill with solar energy and net metering and you currently pay an average of $125 per month in electricity bills, you could save $1,500 per year ($125 x 12 months).

Here Are 23 Ways to Save On Your Electric Bills Right Now

Once you’ve figured out your yearly savings, you can calculate your payback period by dividing the net cost of your system by your yearly savings. A system that costs $15,000 and saves you $1,500 each year, will pay for itself in 10 years.

Here’s the equation written out:

(Solar installation costs – tax credits and other incentives) / (Annual savings) = Payback period in years

Calculate your solar savings

After your payback period, during which time you’re really just recouping your expenses, everything else is savings. Residential solar panels are warrantied for 25 years typically, but their useful life can be much longer. Fifteen years of savings at $1,500 each year is a whopping $22,500.

These calculations are a bit too neat for the real world. Even the most efficient solar panels become less productive over their life span, so you may not get quite as much energy from them in year 25 as in year one (a typical guarantee is between 85% and 92% of its original production).

On the other hand, electricity rates have historically increased fairly steadily. (They’ve gone up about 7% from May 2022 to May 2023, according to the Bureau of Labor Statistics.) This means, in later years, you could be saving even more than you would with solar today.

Like many things, the price of having solar panels installed on your residence has been affected in recent years by inflation and supply chain constraints. According to a report from Wood Mackenzie (PDF), residential solar cost $3.28 per watt to install in the first quarter of 2023, up from $3.07 during the same period in 2022. (Though the report suggests that the price may have started falling again.)

According to CNET sister site SaveOnEnergy, the average cost of a residential solar system as of June 2023 was $31,558 before incentives and rebates, based on a typical solar system size of 8.6 kilowatts. The cost estimate is based on a data set from the Lawrence Berkeley National Laboratory that puts the average solar panel system cost at $3.67 per watt.

Here’s a look at the average cost of a solar panel system for most states, according to FindEnergy.com.

The cost of individual solar installations can vary, however. (Even large scale estimates can vary from source to source, as you see above.) Homeowners can opt for systems of different sizes, with more complexity and extra components, like solar batteries and EV chargers, that bump up the overall cost. Other considerations, like local market conditions and the difficulty of installing solar panels on a certain roof or property, can also affect the final price. And prices can vary from one solar company to the next.

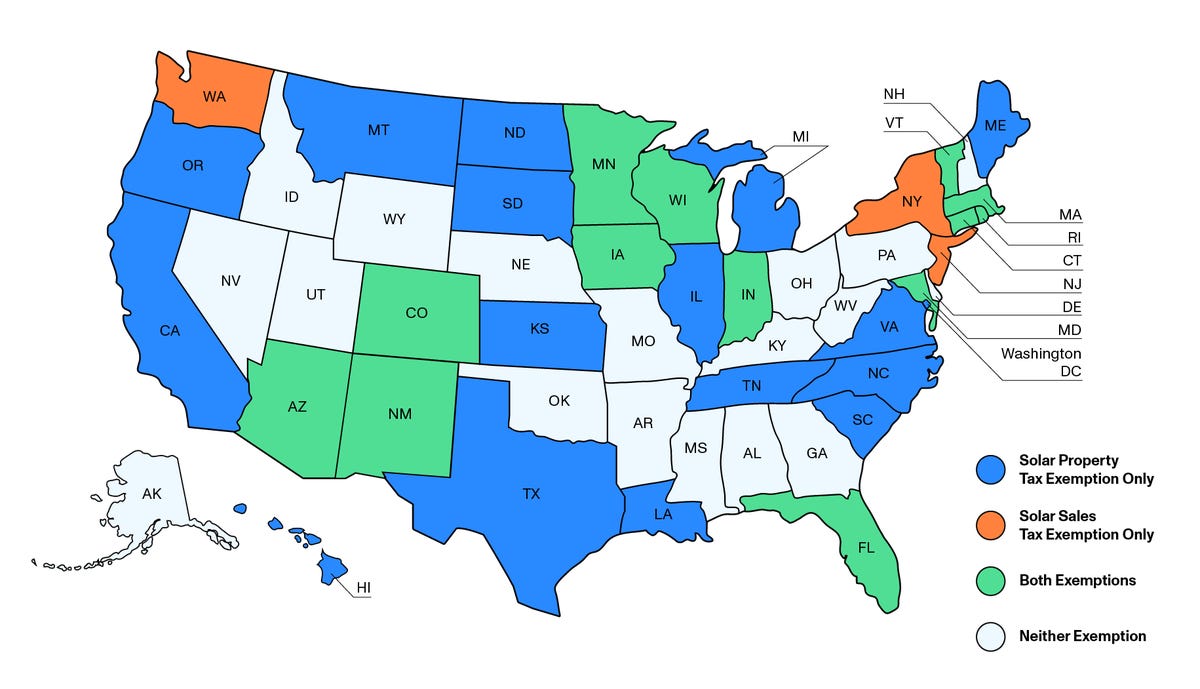

Here’s which states exempt solar panels from sales and property taxes. (Data accurate as of June 6, 2023.)

Zooey Liao/CNET

Beyond such reductions in the upfront cost of installation, using your solar panels over the years can also shrink your energy bill and help pay back your investment through net metering. This is the most popular way utilities compensate homeowners who allow the energy their solar system produces to be fed onto the grid for other consumers to use.

Factors that influence savings

In recent years, net metering policies have begun to shift in some jurisdictions, like the high-profile case in California, and this has sometimes meant a reduction in the overall potential savings from solar. For example, some utilities are moving toward more-complex formulas that govern how much homeowners are paid for releasing energy onto the grid.

It’s important to do your homework to understand your local utility’s net metering policies and any potential changes being considered. You should also get to know any time of use rates that are in place that may influence how much the utility charges for energy consumption and pays for energy production during peak and off-peak hours. In some cases, solar panels paired with a solar battery can save you more with time of use rates than solar panels alone.

Adding an electric vehicle charger is an extra expense, like a battery, but it could increase your savings over time.

The climate and the amount of peak sun hours your location receives can also be a key factor in how much you’ll save over time. A state like New Mexico with up to six peak sun hours per day will obviously allow you to generate more electricity, and possibly save more, than more northern states that receive 25% to 50% less peak sun.

Since solar panels can last 25 years, you need a sturdy roof. If your roof isn’t in top shape, you might have to replace it before installing solar panels. Though you’ll eventually need to replace your roof whether you put solar panels on it or not, having to do so early is an extra expense that might eat into your savings.

Find your state’s solar incentives

Frequently asked questions

Are solar panels really worth it?

The best way to answer this is by doing the math. If you can save more on electricity over time with a solar system than the net cost of installing it, then it’s worthwhile from an economic perspective.

Is it worth paying off solar panels?

Again, this comes down to the numbers. If you’ve financed your solar system and you’re accruing interest on it, it may be advantageous to pay it off as soon as possible.

What are the main disadvantages of solar energy?

The central disadvantage is the upfront cost of a solar installation. Of course, this is partially offset by numerous incentives, like the federal tax credit. Some people may also consider solar panels an eyesore.

What Are Cookies

As is common practice with almost all professional websites this site uses cookies, which are tiny files that are downloaded to your computer, to improve your experience. This page describes what information they gather, how we use it and why we sometimes need to store these cookies. We will also share how you can prevent these cookies from being stored however this may downgrade or 'break' certain elements of the sites functionality.

How We Use Cookies

We use cookies for a variety of reasons detailed below. Unfortunately in most cases there are no industry standard options for disabling cookies without completely disabling the functionality and features they add to this site. It is recommended that you leave on all cookies if you are not sure whether you need them or not in case they are used to provide a service that you use.

Disabling Cookies

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.