One year since the start of the pandemic and the housing industry continues to show resilience. Double-digit home appreciation, low mortgage rates, and the growth of the economic confidence index are things that could not have been forecast in April 2020. That is the reality right now, however.

But what about the real estate market in 2022? What should home buyers, home sellers, real estate agents, and investors expect from the 2022 real estate market?

According to research conducted by major real estate bodies, including Mashvisor’s real estate market forecast and input from some economists and analysts, the housing market will still be growing in 2022. We will also present ideas on how to take advantage of these 2022 real estate market trends if you are a buyer, seller or investor.

To get a US real estate market overview 2022, check out our video below:

Housing Market Predictions 2022: Hot or Cold?

Last year proved how difficult it is to predict real estate. Many people, during the height of the coronavirus pandemic, predicted a housing-induced recession in 2020. In reality, there was an unexpected boom in real estate demand, the likes of which had not occurred since 2006. The fact that the housing sector boomed during a time of short-term hysteria and inflation could be an indicator of how the housing market has evolved. Will this resilience continue in 2022? Or will we see a validation of the many housing market crash predictions in 2022? Taking a look at the factors that influence the 2022 real estate market, we are bullish. Here’s a snapshot of our real estate market forecast:

- The cost of construction will come down a bit. A big part of the problem with the low inventory in the new construction segment was the high cost of production. There is an inflation problem, albeit short-term, affecting the manufacturing industry. This has driven up the prices of building materials for homes and even automobiles. Lumber prices alone added about $36,000 to new home prices. In the 2022 real estate market, bottlenecks in the supply chain will be fixed with continued economic growth, and many companies will restock their shelves.

- Buyers chased out of the market by high prices and bidding wars have waited around for 2022 as the year to pounce. We will see these buyers re-enter the market in droves. Although prices may still be high in 2022, they would probably not appreciate at the high flying rates we witnessed in 2020 and 2021.

- The economic growth that started in the third quarter of 2020 is expected to continue into 2022. The federal reserve’s forecast on real economic growth for 2022 is 3.3%.

We asked some real estate experts, economists, and investors what they think about the 2022 housing market. Will it be hot or cold? Here are the responses we got:

I expect the housing market to remain strong in 2022. While typically a hot market is indicated by rising prices and strong demand, I expect home prices to continue to rise in 2022. We may see a slower growth compared to this year as more inventory will come to the market with fewer COVID-19 restrictions later this year. Low mortgage rates, rising employment, and growing millennial demand will keep the housing market strong. Keep in mind that about 4.6 million millennials will reach the age that millennials typically get married in 2022. Specifically, I expect home prices to rise 9% and 3% in 2021 and 2022, respectively.

Nadia Evangelou, Senior Economist & Director of Forecasting, NAR (National Association of Realtors)

The new construction market continues to be hot, with demand outpacing supply. However, costs of all types of construction materials are rising, which is forcing new home prices higher. In fact, in April, new home prices were up 20% year-over-year according to NAHB. These price gains, reflecting higher costs of construction, are unsustainable and will inevitably price some prospective home buyers out of the market. Consequently, we will see some cooling of these growth rates in the months ahead.

Robert Dietz, Chief Economist, NAHB (National Association of Home Builders)

Housing Market Forecast for Home Buyers in 2022

-

Comparatively Higher Mortgage Rates

Compared to the 2.66% rate seen from December 2020 through January 2021, we will see mortgage rates rise more in 2022. Due to high real economic growth in the first quarter of 2021, which allowed a $1,400 stimulus for individuals under the American Rescue Plan Act, rates are looking up. This means that buyers who were attracted by low mortgage rates may have to take a step back. Rising mortgage rates will create a small dampening effect on demand.

According to Freddie Mac’s estimate, the 30-year fixed mortgage rate will average 3.4% in the fourth quarter of 2021, increasing to 3.8% in the fourth quarter of 2022. This would have a stabilizing effect on price growth as the price-inventory problem continues. Freddie Mac predicts that home prices will rise 6.6% in 2021, slowing down to 4.4% in 2022, while it expects new and existing home sales to reach 7.1 million in 2021 and then decline to 6.7 million homes in 2022.

As expected, mortgage originations will decline in 2022. Refinancing originations will decline from $ 2.65 trillion in 2020 to $1.83 trillion in 2021 and $770 billion in 2022. Single-family mortgage origination activity will decrease from $4.04 trillion in 2020 to $3.48 trillion in 2021 and $2.39 trillion in 2022.

-

Property Values Staying High

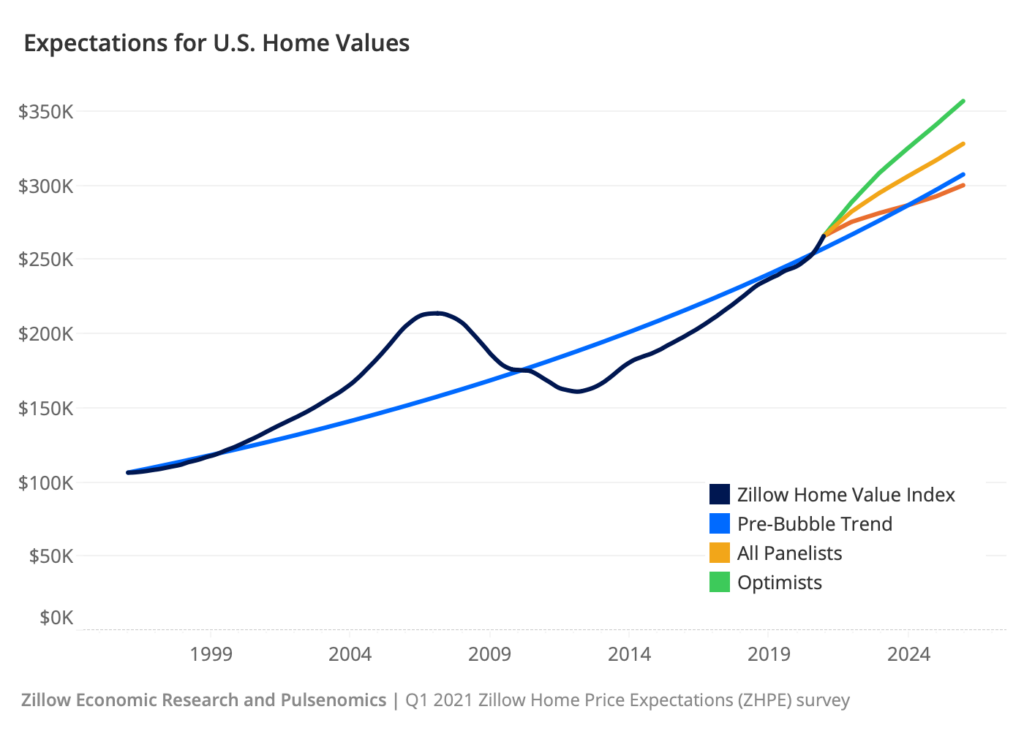

Zillow’s market forecast believes that U.S. house prices would have risen 11.8% by April 2022. Zillow Economic Research predicts that annual home value growth will rise to 13.5% in mid-2021 and that home values by the end of 2021 will increase 10.5% from their current levels. Zillow forecasts that sales volume will remain elevated in the coming year, reaching 6.9 million sales in 2021, the most since 2005.

Home prices are expected to continue appreciating at a historically high rate through the first quarter of 2022. According to experts, the current rise in home prices is similar to the rise in prices that preceded the 2008 recession. Despite the similarities, the circumstances that led to both cases of historic home value growth are quite different.

Data from Realtor.com shows that the median list price of homes nationwide grew 17.2% from last year and reached $375,000 in April, more than last month’s growth rate of 15.6%. The median listing price of $375,000 is a new all-time high. Sales prices in the nation’s largest metropolitan real estate markets grew an average of 11.6% compared to last year, but are slightly lower than last month’s rate of 12.1%.

The double-digit acceleration in home values may significantly drop in the 2022 real estate market. Freddie Mac, at the start of the year, predicted that home values will accelerate by 6.6%. We’ve seen prices accelerate at double this rate in 2021, and prices still trend upwards. In 2022, they predict a 4.4% price increase because an influx of new inventory, especially between the second and third quarter, will stabilize prices.

NAHB’s (National Association of Home Builders) Builder Sentiment measures how builders view the housing market in terms of how much demand there currently is for new homes and how much demand is expected in the future. A score above 50 indicates a favorable outlook for home sales. In April and May 2021, builders’ confidence remained constant at 83, despite the persistent price problem and shortage of construction materials. Builders will need to build 1.1 million to 1.2 million single-family homes to meet long-term demand.

The NAHB, reporting based on data from Random Lengths Framing Lumber Composite, which measures prices based on high volume producing regions in the U.S. and Canada, estimates that lumber prices rose by nearly 250% since 2020. This is one of the reasons for the affordability problem.

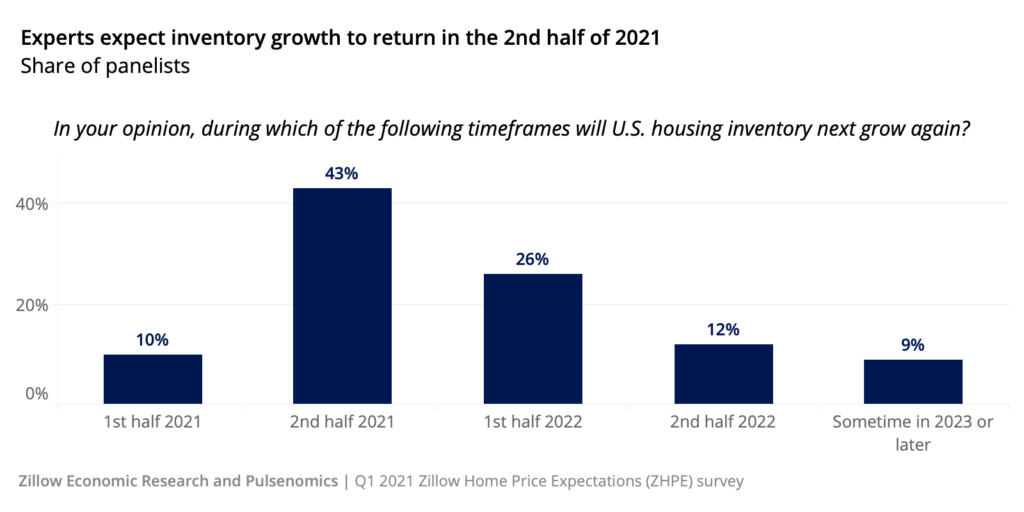

Source: ZHPE Survey

However, as prices for some building materials stabilize in 2022 and builders take in new inventory, we may see new construction flourish. The Mortgage Bankers Association (MBA) expects single-family housing starts to hover around 1.134 million. And that could be just the beginning, as projections in the future are even more optimistic: 1.165 million single-family homes in 2022 and 1.210 million in 2023.

-

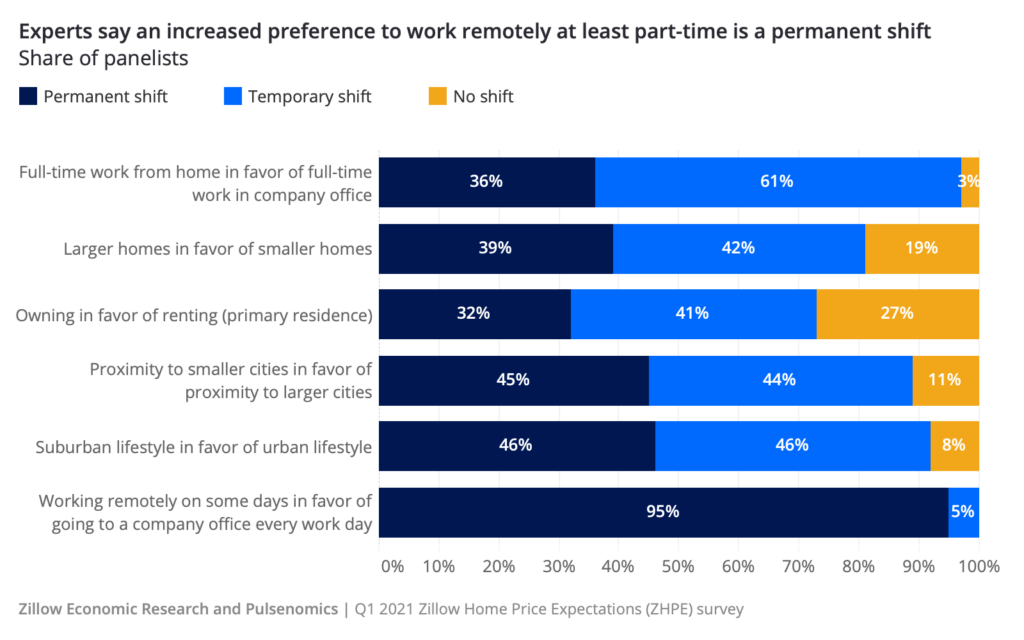

Move to Small Cities Backed by Affordability Concerns and WFH

Cities where real estate is priced within the price range of most first-time buyers will continue to see increased demand.

In a similar manner to people moving away from big, expensive cities like San Francisco, there will also be fewer people moving to cities like Austin where housing prices have risen drastically. As demand shifts, small cities will become much more competitive, leading to comparatively higher price increases.

Hence, our real estate forecast signals a measure of house price compensation across U.S. cities. Downtown homes in the Midwest and South like Memphis, TN, will be some of the best places to look for home buyers and real estate investors in the 2022 real estate market. It might take a while before big city demand returns to pre-pandemic levels as more companies adopt work from home.

Source: ZHPE Survey

Real Estate Projections for Home Investors in 2022

-

Increase in WFH Friendly and Outdoor Amenities

Rentals with outdoor amenities command higher rates on short-term rental websites like Airbnb. This goes to show that people are more interested in spending time outdoors. Single-family and multi-family landlords who prioritize high occupancy and long-term value appreciation might want to invest in outdoor grills, kids playground, exercise rooms garden areas with benches, and luscious green landscapes. Even community HOA recreation facilities are seeing increased foot traffic. We expect that renters and homeowners alike would want to spend more time out to socialize and enjoy the fresh air. And yes, they’ll have more free time with the current work from home trend.

-

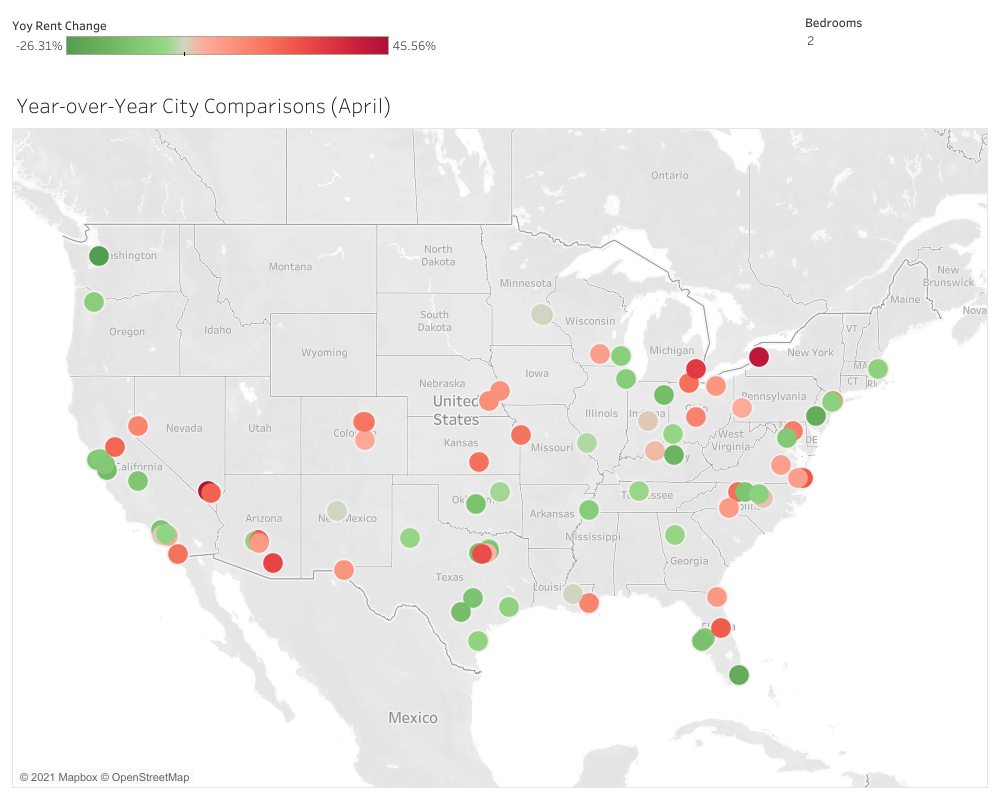

Rent Growth in Some Cities

As home value appreciation slows, rental prices would continue to grow in 2022, eventually outpacing home value growth. As expected, landlords want to recoup the gains lost as a result of the eviction moratorium that was extended for more than 12 months. According to a BusinessInsider article, “shelter inflation, which tracks prices – is forecast to boom just as price growth elsewhere cools.”

“Forecasts suggest that rising shelter inflation could also push inflation expectations permanently higher. Shelter prices are expected to grow by 3.8% year over year by the end of 2022,” Goldman economists said.

Currently, year-over-year rental prices have grown at a comparatively lower rate compared to home value appreciation, leading experts to conclude that renting is still more profitable than buying. If home price appreciation slows in 2022, rental prices could continue to grow.

The national Apartment List Rent Report for June 2021 suggests that rents are still on the rise across the country. The national Apartment List index increased 2.3% from April to May, representing the third consecutive month of record rent growth. Year-over-year rent growth now stands at 5.4% nationally. Cities like Boise, which had the fastest year-over-year rent growth, saw rents rise a staggering 6.6% in June alone. In Boise, rental prices are up 31% since April 2020.

Apartment Guide’s May 2021 Rent Report highlights rental trends and year-over-year price fluctuations that renters may experience in various parts of the United States. They compare rental prices for studio, one-bedroom, two-bedroom, and three-bedroom apartments to determine which unit types and which of the country’s most populous cities are becoming more affordable or more expensive for renters.

The report shows that all unit types reflect price increases since last month, possibly reflecting growing demand. Every apartment type is also increasing year over year, except studio apartments.

Source: Apartment Guide

Riverside was the fastest growing metro area, with median rent reaching $1,950 in April, up 15.0% year over year. The other metro areas topping the list for fastest-growing rents were Sacramento, CA; Memphis, TN; and Tampa, FL, where rents grew by more than 12% compared to last year. As home prices reach record highs, mortgages rise and affordability becomes an issue for prospective homebuyers, the appetite for renting may increase as prospective buyers opt to rent.

-

Rent Control Going into Effect in Some Cities

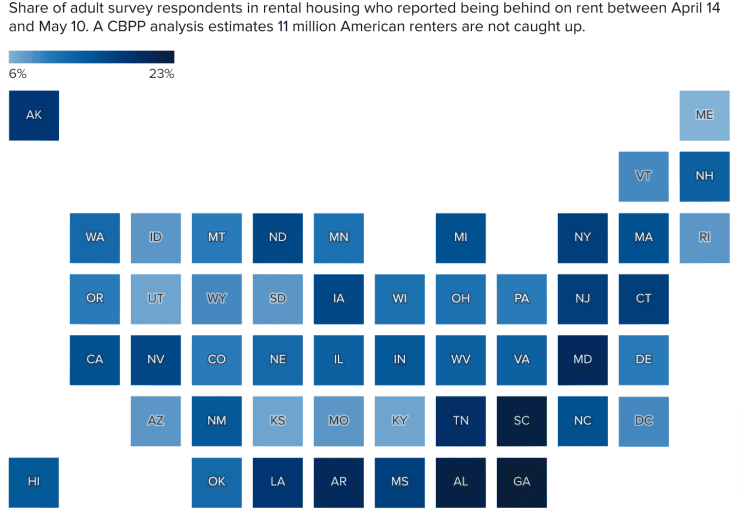

When the federal moratorium on renting expires, policymakers would have to decide how best to prevent a wave of evictions. Currently, nearly 11 million renters have at least one month of missed rent payments.

Source: CNBC

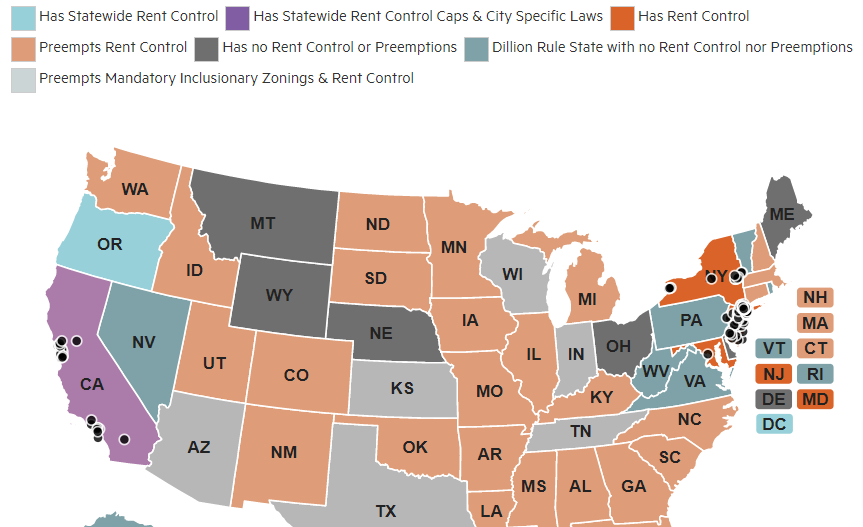

Rent control might be a way to take a stab at the problem. Rent control is already in effect in some U.S. states like DC, New York, and Oregon, even though there are arguments both for and against it. Rent control or rent stabilization laws place a cap on the maximum rent that landlords in a particular state, city, or municipality may charge. Currently, here’s a map showing which states have rent control and which states preempt it. There could possibly be propositions by policy makers in some states to review rent control bans, especially in states with high rates of rent growth.

A major disadvantage of rent control is that when it becomes too much, investors may have to reconsider how much they invest in multifamily apartments and possibly consider converting them to shadow rentals (SFHs, condos, or co-ops).

Source: NMHC

How Should Buyers and Investors Prepare for the 2022 Real Estate Market?

- Start preparing now. The 2022 real estate market might be a lot less hard on buyers than the past 12-18 months, but it’s not going to be a walk in the park. There’d possibly be bidding wars, especially in desirable locations. Buyers and investors can give themselves an edge over the competition by putting themselves in a good position financial-wise. You want to make sure your credit score and DTI (debt to income) is in top shape, and that you have up to 20% down payment savings.

- Stick to a budget. Currently, you would need to raise your budget a bit higher to win the deal if you are interested in buying your dream home or investment property. At the same time, having a ceiling on how high a price you’re willing to pay for a property keeps you objective instead of emotional. Ideally, as a home buyer, you shouldn’t be spending more than 30% of your monthly income on mortgage payments. As a real estate investor, you should also set up an upper limit on much you can afford to spend on monthly mortgage payments. Use an investment property calculator like Mashvisor to figure out how much a home will cost you monthly.

- Always conduct a home inspection. In 2020’s frenzy, some sellers bought money pits (houses that eat up lots of cash on repairs) because they bought without due diligence. When a particular home has more than 10 offers, it’s easy to waive the inspection contingency. Although the 2022 real estate market might not be such a frenzy, real estate projections point to a fair deal of competition. However, make sure you conduct proper due diligence before signing on the dotted line.

Housing Market Forecast for Home Sellers in 2022

-

Sellers Troop into the Market

On April 17, 2021, the national inventory of homes for sale fell 53% below the same period last year.

Source: Realtor.com

One of the reasons sellers have been reluctant to list their homes is due to the unpredictability caused by the coronavirus. In March 2020, no one could have guessed that half of all homes in Manchester-Nashua, NH will be sold in less than 19 days, 1 year later. Currently, Manchester-Nashua, NH remains the hottest market in the U.S., according to Realtor.com’s market hotness statistics, based on the number of days a listing remains active on Realtor.com.

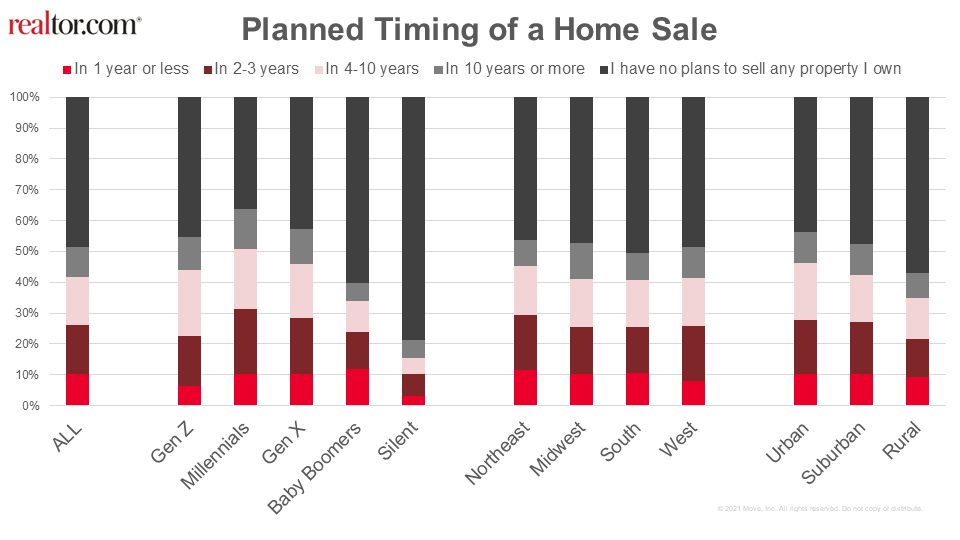

Realtor.com market trends suggest that 10% of all U.S. homeowners would list their homes for sale in the next 12 months.

Source: Realtor.com

With the Federal Reserve planning to keep rates low until at least 2022, homebuyers will have more options to choose from. Much of the real estate-driven economic rebound was due to the Fed keeping short-term borrowing costs low, creating a boomerang effect on all types of interest rates, including mortgage rates. The Fed is also helping to keep mortgage rates low by buying large amounts ($40 billion each month) of agency mortgage-backed securities (MBS) and up to $80 billion in Treasury securities.

However, the low rates will have to come to an end at some point. Bill Gross, Financial Analyst and Co-Founder of Pacific Investment Management Co. says:

When the Fed begins to dial back on its policies, assets that have been supported by low yields, such as Treasury bills and equities, regardless of the growth potential for 2021 and 2022, will be in for a reckoning when they lose that support.

Eliminate low mortgage rates and buyers may need to be incentivized through other means to keep demand high when sellers storm the market.

Jerome Powell, the Fed Chairman, has indicated that the Fed is not even ready to start talking about when it might reduce that support.

We will be looking carefully into the future… When we see that we’re on the right path,” then “we’ll say so, and we’ll say so well in advance of any decision to actually taper.

-

Days on Market Will Increase

Right now, if a home is priced right, there will likely be multiple competing offers. In addition, it would take an average of 25 to 45 days from listing to contract. In May, the average days on market in the U.S. was 39 days. With comparatively less competition and more inventory, days on market will likely increase in 2022. Another reason for the likely increase in days on market is affordability, as the long period of home price growth over the past 12-18 months has left some locations out of reach for some buyers.

-

Home Sellers Facing Foreclosure Can Cash in on Home Equity

Due to the foreclosure moratorium that will end on June 30, there has been a relatively low number of foreclosures. This trend is also supported by banks’ willingness to implement forbearance measures. In March and April of this year, foreclosures have accounted for less than 1% of all home sales, compared to 3% in April 2020.

First-time buyers were responsible for 31% of sales in April, compared to 32% in March and 36% in April 2020. Individual investors or second-time homebuyers, who account for many cash sales, purchased 17% of homes in April, up from 15% in March and 10% in April 2020. Cash sales accounted for 25% of transactions in April, up from 23% in March and 15% in April 2020.

In the first quarter of 2021, lenders began the foreclosure process on 17,652 U.S. properties, up 3% from the previous quarter but down 78% from a year ago. Nationwide, 1 in 4,078 housing units had a foreclosure filing in the first quarter of 2021. There were 7,320 foreclosure default properties repossessed through foreclosure (REO), up 14% from the previous quarter but down 875 from a year ago.

Over the past four quarters, 5.4% of homeowners missed four or more mortgage payments, while more than 3% of homeowners missed 2-3 payments. Obviously, there could be a wave of foreclosures in 2022. But homes today command higher prices. In April, 52% of homes sold above list price. According to ATTOM Data, RealtyTrac’s parent company, about 70% of homeowners have more than 20% equity and more than 90% of borrowers in default have at least 10% equity in their homes. This presents a get-out-of-jail-free card for distressed homeowners.

How Should Sellers Prepare for the 2022 Real Estate Market?

- Price your home right. An appraiser or real estate agent can help you determine the right price. Your home will get stale on the market if you overprice it. One tactic sellers in today’s market use to amass offers and spark bidding wars is underpricing their homes slightly and going with the highest bidder. This might still work in 2022.

- Work on your curb appeal. Sight unseen purchases might reduce in 2022 with the spread of the COVID-19 vaccine. Some potential buyers would want to drive by your house. Your home’s curb appeal would help create a good first impression.

- Sell first before buying. Buying a home and selling a home simultaneously can be tricky since the real estate market favors selling over buying. Due to the shortage of inventory in 2022, finding a home that fits your criteria at your desired price could be a slow process. On the other hand, you could use the cash you earn by selling first to compete during the home search.

- Strike bargains. In the low inventory environment, sellers hold the cards. If you probably want to re-rent the home after it sells or include a contingency that allows you to stay in your home until you find a new one, you can do so.

Where Are Home Prices Expected to Rise in 2022?

According to Zillow’s housing market outlook, prices will keep rising in most of the nation’s cities in 2022, yet at a slower rate. Considering demand and supply factors, home prices is going to rise in the following 7 places, based on Mashvisor data and Zillow’s YoY home value changes (April 2020-April 2021):

1. Memphis, Tennessee (Shelby County)

- YOY Home Value Change: 16.2%

- Median Property Price: $281,156

- Average Traditional Rental Income: $1,093

- Average Traditional Cash on Cash Return: 2.77%

- Average Airbnb Rental Income: $2,590

- Average Airbnb Cash on Cash Return: 4.66%

- Average Airbnb Occupancy Rate: 66.52%

2. Riverside, California (Riverside County)

- YOY Home Value Change: 16.5%

- Median Property Price: $575,242

- Average Traditional Rental Income: $2,165

- Average Traditional Cash on Cash Return: 2.35%

- Average Airbnb Rental Income: $4,824

- Average Airbnb Cash on Cash Return: 5.52%

- Average Airbnb Occupancy Rate: 65.3%

3. Phoenix, Arizona (Maricopa County)

- YOY Home Value Change: 21.2%

- Median Property Price: $523,779

- Average Traditional Rental Income: $1,588

- Average Traditional Cash on Cash Return: 2.08%

- Average Airbnb Rental Income: $3,311

- Average Airbnb Cash on Cash Return: 3.90%

- Average Airbnb Occupancy Rate: 66.59%

4. Sacramento, California (Sacramento County)

- YOY Home Value Change: 15.6%

- Median Property Price: $454,560

- Average Traditional Rental Income: $1,646

- Average Airbnb Cash on Cash Return: 1.98%

- Average Airbnb Rental Income: $3,534

- Average Airbnb Cash on Cash Return: 4.92%

- Average Airbnb Occupancy Rate: 74.09%

5. Charlotte, North Carolina (Mecklenburg County)

- YOY Home Value Change: 14.9%

- Median Property Price: $499,199

- Average Traditional Rental Income: $1,765

- Average Traditional Cash on Cash Return: 2.16%

- Average Airbnb Rental Income: $2,548

- Average Airbnb Cash on Cash Return: 2.49%

- Average Airbnb Occupancy Rate: 58.07%

6. Columbus, Ohio (Franklin County)

- YOY Home Value Change: 14.2%

- Median Property Price: $293,618

- Average Traditional Rental Income: $1,225

- Average Traditional Cash on Cash Return: 2.67%

- Average Airbnb Rental Income: $1,903

- Average Airbnb Cash on Cash Return: 3.37%

- Average AirBnB Occupancy Rate: 58.37%

7. Austin, Texas (Travis County)

- YOY Home Value Change: 25.5%

- Median Property Price: $733,314

- Average Traditional Rental Income: $2,005

- Average Traditional Cash on Cash Return: 0.95%

- Average Airbnb Rental Income: $3,936

- Average Airbnb Cash on Cash Return: 2.89%

- Average Airbnb Occupancy Rate: 59.31%

Source: ZHPE Survey

COVID-19 and Its Effect on Prices of Building Materials

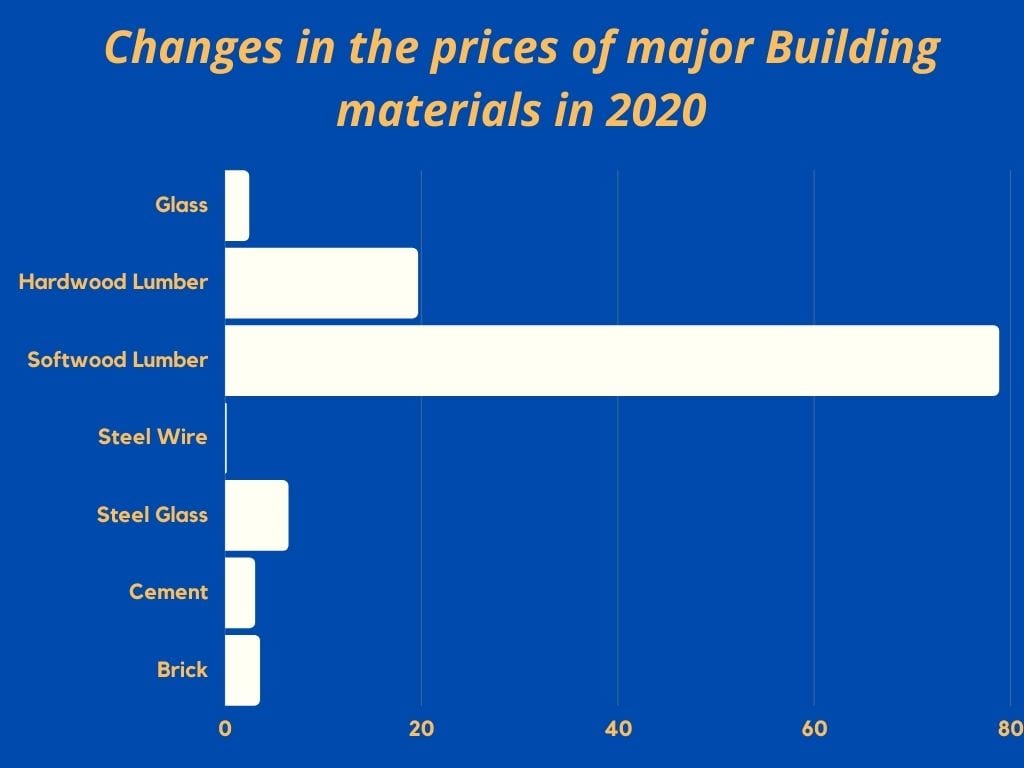

COVID-19 caused a lot of disruption in many industries. The housing industry and the building materials industry were one of the hardest hit. But while housing has bounced back robustly, construction is still trying to gather steam. Not only has it been hard to find labor subsequent to the COVID-19 lay-offs, but the prices of almost all building materials have increased. In order to better understand how prices for homebuilding materials changed during COVID-19, UpNest analyzed Federal Reserve Economic Data (FRED). Some of the reasons for scarcity in building materials aren’t directly tied to COVID-19.

While production slowed down during the COVID-19 pandemic and the consequent restrictions, there were also supply chain issues from wildfires and low supply of labor. The result is the increase in new construction home prices. Softwood Lumber (78.8%) saw the most gain in price majorly due to a slowdown in production and its use for DIY home remodeling projects, while the price of steel wire (0.1%) didn’t change notably. Experts predict that lumber prices will drop considerably in 2022.

Data Sout Data Source: SCNOW

Data Source: SCNOW

Housing Bubble 2022: Will the Housing Market Crash in 2022?

There are three major reasons why there will probably not be a housing market crash in 2022:

1. Inventory is low.

Unlike 2008, inventory has declined to critical levels. The U.S. housing industry is 3.8 million single-family homes short of what is needed to meet the country’s housing demand, up 52% as compared with 2018’s shortfall, according to a new analysis from mortgage-finance company Freddie Mac. In 2018, Freddie Mac had estimated that the housing market was 2.5 million units short of what it needed to meet long-term demand. The new estimate is as of the end of 2020, and it emphasizes the severity of the housing supply.

While low inventory is a problem, it also creates an opportunity for home equity to rise, and hence the 2022 real estate market is likely going to be a seller’s market. This means a housing market crash isn’t likely to happen in 2022.

2. Lenient forbearance terms and home equity.

The Federal Housing Finance Agency (FHFA), Fannie Mae, and Freddie Mac announced new payment deferral options in June 2020. Borrowers who can return to making their normal monthly mortgage payments may choose to defer their missed payments until they sell or refinance their home, or until mortgage maturity.

FHFA Director Mark Calabria said:

For homeowners in forbearance due to COVID-19, payment deferral allows them to make up missed forbearance payments when they sell their home or refinance… This new forbearance repayment solution responsibly simplifies options for homeowners while providing an additional tool for mortgage servicers. Borrowers who can pay their mortgage should, because missed payments remain an obligation that will ultimately have to be repaid.

3. The economy continues to grow

The Bureau of Labor Statistics (BLS) publishes an occupational outlook each year that goes into great detail about each industry and occupation. Overall, the BLS expects total employment to increase by 6 million jobs between 2019 and 2029. Manufacturing and retail industries will continue to shed jobs, while e-commerce continues to grow.

A 2013 prediction by the BLS expects that from 2012 to 2022, GDP will grow at a rate of 2.6% per year, reaching $17.6 trillion in the target year of the projections. The unemployment rate is projected to gradually decrease to 5.4%, accompanied by a gain in household employment of 12.3 million jobs.

Diane Swonk, Chief Economist at Grant Thornton, said she expects 2021’s growth rate to be 6.6%, the strongest year since 1984. She expects 4.3% annualized pace of growth for Gross Domestic Product in 2022.

Real Estate Market Forecast: Housing Affordability Will Be the Problem

In a new report from the Urban Institute, researchers found that over the next two decades the U.S. homeownership rate could decline to 62.1%. They project that the overall homeownership rate will fall from 65% in 2020 to 62% by 2040.

Household growth averaged 12.4 million per decade between 1990 and 2010, and 7.3 million between 2010 and 2020. They estimate an average growth of 8.5 million from 2020 to 2030 and 7.6 million from 2030 to 2040. This decline is the result of slowing U.S. population growth AND lower headship rates for most age groups.

Another key finding is that renter growth will more than double the rate of homeownership growth from 2020 to 2040. Between 2020 and 2040, there will be 9.3 million net new renter households, an increase of 21%.

The number of families spending more than 50% of their incomes on mortgages or rent has significantly increased. Rising building materials cost and low inventory is pricing first time buyers and investors out of desired locations and this may be the real issue. California housing market predictions 2022, for example, indicate steadily rising home prices. It is likely that many people who have waited to buy in 2022 will have to buy their dream home at the high end in 2022 if mortgage rates remain low.

When Will the Housing Market Crash?

The good news is that the real estate forecast next 5 years by many analysts is that we aren’t going to witness a housing market crash. The more likely scenario is that price growth will slow down till normalcy is reached. But when will housing prices drop?

Earlier this month, the property data and analytics company CoreLogic published a housing market update that focused on prices. According to their real estate market forecast:

Nationally, home prices increased 10.4% in February 2021, compared with February 2020… Home prices are projected to increase 3.2% by February 2022.

This 3.2% price appreciation projection is close to the normal rate of price appreciation in a stable market. Based on CoreLogic’s prediction, it appears we will see the frenzied rate of growth witnessed in the recent past stabilize in 2022.

Will Home Prices Come Down in 2022?

We do not think home prices will come down in 2022. Experts forecast a slow down in price appreciation, but the imbalance in demand and supply will keep home prices up.

This real estate market forecast offers projections on what we think the 2022 real estate market will be like. However, it is a prediction. Just as 2020 taught us that nothing is certain, this real estate market forecast is not set in stone. But it can help guide you as you plan towards navigating the housing industry in 2022 either as a real estate buyer, a realtor, or an investor.

And if you’re looking to buy an investment property in 2022, now would be the best time to start planning. Want to view and analyze top performing investment properties? Check out the Mashvisor real estate software platform.