Amid increased mortgage rates, finding the best loans for investment property is crucial for the success of a real estate business in 2023.

How you finance the purchase of a rental property is always important as it affects the size of the investment, which in turn impacts the rate of return. However, it has become even more important in recent months, as a result of rising interest rates. It has made the financing of investment properties more expensive.

Table of Contents

- What Is an Investment Property Loan?

- Is It Advisable to Take Out a Loan to Buy an Investment Property?

- 7 Best Loan Types for Investment Property

- How to Find an Investment Property

- Getting Started With the Best Loans for Investment Property in 2023

Beginner real estate investors mistakenly consider conventional mortgage loans to be the only or at least the predominant option. The truth is that there are various types of bank and other loans that make sense for investors and that allow for buying the best investment property.

In this article, we will define an investment property loan and discuss when it’s a good idea to take out one to purchase a rental. We will focus on the most appropriate varieties of loans for investors and their needs, covering both the pros and cons as well as the interest rates you can expect at the moment.

We’ll cover the following types:

- Conventional mortgage loans

- FHA loans

- VA loans

- Hard money loans

- Private money loans

- HELOCs

- Crowdfunding

Lastly, we will show you how to identify and buy top-performing long term and short term rental properties across the US market, regardless of your financing solution. The tools available on the Mashvisor platform can help you locate both excellent markets and ideal properties for real estate investing.

What Is an Investment Property Loan?

An investment property loan is exactly what it sounds like. It is money that you borrow to finance the purchase of a property that you buy for investment purposes, which makes it different from your primary home.

Usually, the investment property is a long term or short term rental property. However, sometimes, investors also borrow money to finance house flipping projects or even real estate development works.

As a matter of fact, in many cases, real estate investors have more loan options available to them than homebuyers. While the latter is generally limited to conventional mortgage loans and their variations, property investors can tap into significantly more types of financial resources.

So, in case, as a beginner investor, you’re wondering, “Is it hard to finance an investment property?”, chances are that you will be able to find a loan that addresses your specific needs. All that’s required is a bit of research on the best loans for investment property and talking to a few different banks and other lending institutions as they all offer varying terms and conditions.

Is It Advisable to Take Out a Loan to Buy an Investment Property?

Taking out a loan to buy an investment property is often a necessity. The majority of investors, especially beginners, do not have enough saved capital to purchase an entire rental property out of pocket. So, they need to resort to the money of other financiers or other investors.

Indeed, it’s one of the most significant benefits of investing in real estate. You can use the money of others to make money for yourself in the short term (through rental income) and in the long term (through real estate appreciation). Having said that, you must proceed with caution when taking out a loan and always search for the best loans for investment property.

Some factors to take into account include the following:

- The loan type

- The loan term

- The loan structure

- The interest rates

- The financing institution (a bank or another lending organization)

The reason why you should be so careful in selecting the right loan type and structure is that financing plays a major role in most measures of return on investment in real estate. Particularly, it is directly present in the cash on cash return formula, which evaluates the ROI of rental properties in the most comprehensive manner.

Moreover, the loan you take out to buy an income property also affects the feasibility and stability of your rental business. Even if you buy the best investment property in the best real estate market, things can go downhill if you cannot afford to pay the monthly mortgage. You can end up in foreclosure and lose your property altogether.

But if you do your loan research and investment property analysis diligently, taking out a loan is definitely advisable to start making money from real estate.

7 Best Loan Types for Investment Property

Now that investors know that taking out a loan to purchase a rental property can be an excellent idea, many are thinking: “What loan is best for an investment property?” And this is the exact question that we will tackle in this section. We will cover the loan types most suitable for investors and their properties, including the advantages and disadvantages of each type.

So, what type of loan is best in 2023?

1. Conventional Mortgage Loan

The first type of loan that real estate investors have access to is the conventional mortgage loan. Similar to financing the purchase of a home, this investment loan is usually borrowed from a bank, which can be a large national bank or a small local bank. The term, the structure, and the interest rate can vary depending on the bank and your particular financial situation.

Mortgage loans can be divided into two broad categories: fixed-rate mortgages (FRM) and adjustable-rate mortgages (ARM). In the first case, you agree to pay the initially set interest rate for the rest of the loan duration. In the second case, the rate might be changed in a few years to reflect the current situation in the mortgage market.

If you’re wondering, “Is it easy to get a loan for an investment property?”, the truth is that it is a bit harder than qualifying for a mortgage loan for your home. That’s because investors are seen as riskier borrowers than homeowners. In case of financial hardship, you’re more likely to pay your home mortgage first and your investment property loan second.

Pros of Conventional Mortgage Loans

The main benefits of using a mortgage to buy an investment property are:

- Many different options: With mortgage loans, you can choose between various terms, structures, and other factors. So, adapting the loan to the specific needs of the long term or short term rentals for sale that you are buying is feasible.

- Lending institution reliability: Most mortgage lenders are national, regional, or local banks with an established reputation in the market. They are very likely to hold on to their side of the deal.

- Applicability to most investors: Unless you have a terrible credit history, you are likely to qualify for a mortgage loan. And if you cannot maintain a good credit score, it might not be a good idea to invest in real estate, which requires superior financial planning.

- Long term: In most cases, conventional mortgages last 15 to 30 years, which translates into small monthly payments. It makes such types of loans easier to repay and less risky and does not impact the ROI so much.

- Flexible real estate strategy options: While some of the best loans for investment property are limited to buying a home, conventional mortgages can be used for purchasing a rental property. There are no limitations in this regard, so you can go for long term rentals or Airbnb for sale.

- Access to the best markets for real estate investing: Conventional mortgage loans are not subject to geographical restrictions on. It means that you can live in one location and borrow money to buy an investment property in another one. So, you can aim for the top markets for your preferred rental strategy.

Related: 20 Best Places to Invest in Real Estate in 2023

Cons of Conventional Mortgage Loans

Meanwhile, the most significant drawbacks of mortgages include the following:

- Sizable down payment: If you’re thinking, “Can I put less than 20% down on an investment property?”, the answer is no. It’s the minimal down payment requirement for most conventional mortgages when buying an investment property (not a home).

- Potentially high mortgage rates: Since the beginning of the year, the interest rate on mortgages has gone up significantly, reaching 5.67% for a 15-year FRM and 6.33% for a 30-year FRM at the moment. The rates were even higher in October and November 2022, and they are not expected to go below the 5% threshold throughout 2023.

- Credit score requirements: The minimum credit score needed for a conventional mortgage is around 620, which might pose a challenge for some investors. But if you cannot take care of your credit score, chances are you might not be able to manage an investment property.

2. FHA Loan

The second type of loan you can take out to buy an investment property is an FHA loan. It is a government-backed mortgage that comes with looser requirements. So, it may give access to financing to borrowers who do not qualify for a conventional mortgage loan.

However, the trap is that an FHA loan applies only to buying a primary residence and not a second home, a rental property, an income property, or an investment property. But you might be able to get around this requirement if you don’t own a home yet and decide to go for house hacking.

House hacking is a real estate investment strategy for beginners in which you purchase a small multifamily home to live in one housing unit and rent out the rest. Duplexes, triplexes, and quadruplexes are ideal for this purpose. You can rent out the available housing units on a long term or short term basis.

Related: How to Make Big Money With Small Multifamily Real Estate Investing

So, in case you’re still wondering, “Can I put less than 20% down on an investment property?”, the answer is: Yes, with an FHA loan.

Pros of FHA Loans

FHA mortgage loans provide some important benefits over other best loans for property investment, including:

- Low down payment: FHA loans lower the minimum down payment requirement from 20% to only 3.5%. It means that investors require less capital to get started in real estate.

- Low interest rates: In mid-December 2022, the 30-year FHA rate is 6.07%, a bit below the prevailing conventional mortgage rates. It makes repaying an FHA loan more affordable.

- Low credit score: With a credit score as low as 580, you can put down 3.5% of the property price. The required credit score for an FHA loan can go down to as little as 500 if you can make a 10% down payment.

Cons of FHA Loans

Using an FHA loan to purchase an income property comes with a few downsides, such as:

- Limited real estate investing strategy options: FHA loans can be used to buy a primary residence exclusively. Investment properties do not qualify. Again, you can opt for house hacking if you don’t own a home at the moment and if you’d like to invest in the market where you live.

- Limited loan size: In 2022, the upper ceiling for an FHA loan for a single family home is limited to $420,680 in a low-cost area and $970,800 in a high-cost area. The ceiling is expected to stay the same in 2023. With a US median property price close to $360,000, investors might face limited options, especially when buying multifamily properties.

- Mortgage Insurance Premiums: An FHA loan requires both upfront and annual mortgage insurance premiums (MIPs). It is a necessary mortgage insurance paid by the borrower to protect the bank or another lender from potential defaults on monthly payments. It is a must because of the less strict qualification requirements.

3. VA Loan

Another financing option worth considering in 2023 is a VA loan. It is a government-backed mortgage available to veterans, service members, and surviving spouses. Consequently, it can meet the needs of only a certain type of real estate investors. Nevertheless, the terms and conditions are very favorable.

Similar to an FHA loan, VA loans must be used for buying a primary residence. Again, rental property investors can get around the said requirement with the house hacking strategy. However, they need to conduct careful real estate market analysis to ensure that their location is good for long term or short term rentals in small multifamily homes.

Related: House Hacking: How I Got Started in Real Estate at 23

Pros of VA Loans

The main advantages of this type of investment property loan include the following:

- No down payment: The US Department of Veteran Affairs does not ask for a down payment on VA loans, which makes access very easy even for first-time investors.

- Low interest rates: VA loans offer lower mortgage rates than other best loans for investment property. Currently, the interest rates are 5.25% for both a 15-year and a 30-year fixed VA purchase. It is significantly less than the conventional mortgage, as well as the FHA loan interest rates.

- No credit score requirement: The VA does not require a minimum credit score for VA loan eligibility.

- Limited closing costs: The closing costs of VA loans are lower than the closing costs of conventional mortgages. It is an important benefit to make financing an investment property more affordable.

- No Private Mortgage Insurance (PMI): With a VA loan, there is no need for Private Mortgage Insurance (PMI), helping lower the investment cost.

- Multiple uses: It is considered a lifetime benefit, meaning that eligible borrowers can use a VA loan over and over again as they meet the eligibility criteria.

Cons of VA Loans

Meanwhile, the disadvantages of this loan type are:

- Lenders imposing down payment requirements: While the VA does not require a down payment, banks and other financial institutions giving the loan might have such a requirement. It’s worth checking out a few different institutions to select the best option for your particular needs.

- Lenders imposing credit score requirements: The VA Department does not expect a minimum credit score, but it cannot prevent lending institutions from doing so. In many cases, banks expect a credit score of 620 or more to give out a VA loan. It makes such types of loans comparable to conventional mortgages.

- Limited investment options: VA loans are meant to give veterans access to homeownership, so technically you cannot purchase an income property with one. But you can use a VA loan to get into real estate investing if you opt for house hacking. Just do a rental market analysis to ensure that investing in your location makes sense.

4. Hard Money Loan

A type of loan that homeowners do not have access to but real estate investors do is hard money loans. They are short term, non-conforming loans that come from private individuals or companies and not traditional financing institutions like banks. They use the investment property as collateral, which allows them to offer a more flexible loan structure and terms.

Because hard money lenders usually lend money for significantly shorter periods than conventional banks, this type of loans are generally used for flipping houses. However, there is no official restriction on the real estate strategy, so they can be used to buy an investment property to rent out.

Pros of Hard Money Loans

The main pros of borrowing money from hard money lenders include the following:

- Flexible down payment requirements: There is no universal requirement for a minimum down payment among hard money lenders. The exact percentage depends on the specific lender and the deal between the lender and the borrower (the real estate investor).

- Flexible credit score requirements: There doesn’t exist one single minimum credit score requirement to qualify for a hard money loan. This sets these loans apart from conventional mortgages.

- Looser qualification requirements: The main advantage of hard money loans is that they have more flexible and adjustable terms than other best loans for investment property. A lot of the terms and conditions depend on the negotiations between the borrower and the hard money lender.

- Asset-based qualification: To approve a borrower, hard money lenders look at their real estate assets rather than financial assets and credit history.

- Shorter time commitment: With a conventional mortgage, an investor commits to repaying over a period of 30 years. On the other hand, with a hard money loan, the repayment period is usually one to three years. It means that in just a couple of years, you will be debt-free, making this loan ideal for serial real estate investors.

- Fast approval: Getting approved for a conventional mortgage loan usually takes two to six weeks, but it might require even more. Receiving approval for a hard money loan can happen in a couple of days.

Cons of Hard Money Loans

At the same time, the risks associated with taking out a loan from a hard money lender include the following:

- High interest rates: Because of the shorter loan term duration and the less stringent eligibility criteria, hard money lenders usually charge an interest rate of 8%-15%. It is needed to compensate them for the higher risk of lending to investors who might not qualify for a conventional mortgage.

- Potentially high down payment: Hard money lenders typically ask for a lower loan-to-value ratio, so down payments usually range between 10% and 35% of the price of the investment property. Thus, hard money loans are ideal for investors with good initial capital who need just a few extra thousand dollars.

- Short time to repay: In most cases, a hard money loan must be repaid in one to three years. It puts lots of pressure on the borrower, who need to ensure the investment property will generate enough income to cover the loan. This loan type should be used for properties with a very high rental rate.

- Investment property as collateral: The largest risk of borrowing from hard money lenders is that the loan uses your investment property or another real estate asset as collateral. If you cannot afford to repay the loan, you will lose your investment.

- Potential requirements for successful track record: Some lenders ask for a proven track record of successful real estate investments using hard money to give another loan. So, this loan might not be good for first-time investors.

- Lack of national reputation: Banks that give conventional mortgages usually have a strong national presence and reputation. Meanwhile, hard money lenders are generally smaller in scale and less reputable. Investors need to do a lot of due diligence and research before trusting a specific hard money lender.

5. Private Money Loan

Another type of financing that can be used to buy vacation rental property or long term rental property is a loan from private money lenders. Private money loans are considered one of the best loans for purchasing investment property. It is because they have even more flexible and less strict requirements than hard money loans.

Private money loans are money that is lent to real estate investors by private people or companies that are even less established and usually smaller scale than hard money lenders. A great dose of creativity goes into coming up with the terms and conditions of a private money loan, which might turn out to be a double-edged sword.

Private money lenders are very different from banks and other major financial institutions. Sometimes, they might even be family members, friends, or other real estate investors with more significant capital.

Pros of Private Money Loans

This type of loan offers the following benefits:

- Very flexible terms: Among all options available for the purchase of an investment property, private money loans are the least structured ones. The terms and conditions depend entirely on the specific lender and the agreement between the borrower and the lender.

- Very loose eligibility requirements: In most cases, there are criteria for qualifying based on the financial situation of the borrower. Thus, real estate investors with shaky credit history can access this type of financing.

- Qualification based on assets: Private money lenders look at the real estate assets – the investment property – rather than the financial assets of the borrower. It makes eligibility easier and broader.

- Quick approval: A private money lender usually needs just a few days to approve a loan. It means that an investor can move forward with the purchase process quickly before losing the deal to another buyer with more ample financial resources.

- Easy repetition: Private money loans have very short terms, which makes them an ideal option for investors looking to build large real estate investment portfolios. As long as they repay one loan, investors can take out the next one to buy a new investment property.

Cons of Private Money Loans

The most significant drawbacks of private money loans are:

- High down payment: There is no official requirement for the minimum size of the down payment with this type of loans, but it can easily reach 30% or even more. It means that a private money loan is a good option for investors who already have significant savings.

- High interest rate: There are no nationwide interest rates for private money lenders, so each lender sets up their own rate. In general, the private money loan interest rates fall in the range of 7%-36%.

- Very short loan term duration: Similar to hard money loans, private money comes with a very short repayment period, in most cases up to 12 months. Sometimes, borrowers might be able to negotiate a loan term duration of two to five years, depending on the lender.

- High risk: Private money loans come with a very high risk. Due to high interest rates and short repayment periods, they are good for very solid real estate investments only, with high rental income and ROI. Alternatively, borrowers might lose their investment property as collateral. Also, private money lenders are less trustworthy than banks.

6. HELOC

Yet another option to finance a rental investment property is a home equity line of credit (HELOC). This loan type is available to homeowners who would like to use the equity they have in their home to finance the purchase of an income property. It is done by turning your home equity into a line of credit.

A HELOC is a relatively more complicated option than other best loans for investment property and might face more restrictions. Thus, it’s important for investors to conduct diligent research before opting for this type of investment property loan.

Pros of HELOCs

The most important benefits of using a HELOC to buy an investment property include the following:

- Access to funds over a long term: With a HELOC, you can continue withdrawing funds year after year. As long as you repay your debt on time, you can use this loan type on a continuous basis. The draw period usually lasts 10-15 years.

- Long repayment period: The repayment period for a HELOC generally ranges between 10 and 20 years. The longer repayment period puts less pressure on real estate investors than options like hard money or private money loans.

- Interest payments on actual withdrawals: An important advantage of this loan is that you pay interest only on the money you withdraw, not on the entire line of credit. It limits the overall cost to borrowers (investors).

- No down payment: There is no need for a down payment as you borrow money against the equity you have on your home. This is a major difference between HELOCs and mortgage loans like a conventional mortgage, FHA loans, and VA loans.

- Tax deductions: Sometimes, investors can deduct the interest costs of a HELOC on their federal tax return. It means that they might be eligible for major savings through tax benefits.

- Access to large amounts of money: With a HELOC, you might be able to borrow a significant amount of funds. Some lenders offer as much as $500,000 through this loan type.

Cons of HELOCs

Meanwhile, investors should keep in mind the following drawbacks before using a HELOC:

- Homeownership requirement: To be eligible for a HELOC, you need to own a home first. Moreover, that’s not enough. You also need to hold a significant amount of equity in your home to be able to turn this into a line credit for purchasing an investment property. Moreover, in most cases, this loan can be used to cover the down payment only.

- Fluctuating interest rates: The interest rate on a HELOC is not fixed for the duration of the loan. Usually, the interest rates are tied to a prime rate and adjusted when the latter goes up or down. The flexible rate makes financial planning more challenging for rental property investors.

- Prepayment penalties: In many cases, closing a credit line faster than planned is associated with paying penalty fees. This is something you should consider in your rental property analysis before borrowing this type of loan.

- Ongoing fees: Frequently, HELOCs require annual fees such as maintenance fees, transaction fees, and other fees, which add up to the overall cost. Make sure to consider these expenses before using a HELOC to buy an investment property.

- Home at risk: The main disadvantage of a HELOC is that investors put their own homes at risk. While hard money and private money lenders use your rental property as collateral, with HELOCs, your home is used as collateral.

7. Crowdfunding

The final type of financing that investors can use to buy an investment property in 2023 is real estate crowdfunding. It’s an option that’s been gaining popularity in recent years among investors who cannot afford to pay for an entire property or who’d like to diversify their investment portfolio.

It’s been largely enabled through advancements in real estate technology, including the introduction of blockchain technology in the real estate industry. So, generally speaking, crowdfunding is an ideal option for tech-savvy real estate investors with at least some basic understanding of technology.

Real estate crowdfunding platforms have made processes relatively straightforward to provide access to just about anyone. But we still think it’s a good idea to have some beginner knowledge of technology before you opt for it.

Actually, crowdfunding is more of its own real estate investing strategy in which small amounts of funds provided by a large number of investors are drawn together to invest in properties. They can be residential or commercial real estate assets. Crowdfunding is a new twist to the old concept of Real Estate Investment Trusts (REITs) but with lower initial capital requirements.

Pros of Crowdfunding

The main pros of real estate crowdfunding are:

- Extremely low initial capital requirements: Most of the best loans for investment property in 2023 require investors to put down at least 3.5% of the property price. In most cases, the minimum down payment is above 20%. With crowdfunding, you can start investing in real estate for as little as $50, depending on the platform.

- Real estate investment portfolio diversification: Because of the low initial investment and the lack of personal involvement, investors can invest in numerous real estate crowdfunding platforms simultaneously. This strategy is one of the fastest ways to diversify your portfolio.

- Low risk: Crowdfunding is very low risk as it requires very small investments (amounts you can afford to lose), and it is professionally managed by real estate experts.

- Passive real estate income: Many go into real estate investing for the potential for passive income. With crowdfunding, this benefit is a given. Once you choose a platform, you don’t need to do anything related to the management of the actual investment properties.

- Access to commercial real estate assets: Most first-time investors can only afford to purchase residential properties, while crowdfunding gives them access to commercial-grade properties. It is part of the democratization of the real estate market that technology has enabled.

Cons of Crowdfunding

The most significant downsides of crowdfunding that investors should consider include the following:

- Limited return on investment: When you buy your own rental property, you can make a few thousand dollars per month. With crowdfunding, your return is much less because you invest significantly less and you don’t own the entire investment property.

- No control over property management: Investing in real estate with multiple other owners whom you don’t even know means that you get zero control over the management of the property. It is handled by the team of the real estate crowdfunding platform. This is a drawback for investors with knowledge of the industry and the market.

- Relatively new strategy: Crowdfunding has been around for just a few years, and most PropTech companies offering this option are still small-scale startups. So, investors are advised to proceed with caution and relatively small investment amounts before this strategy is able to prove its reliability and trustworthiness.

How to Find an Investment Property

Now that you know the best loans for investment property in 2023, let’s look at the process of finding good rental properties. After all, securing a good financing option is just one of the requirements of starting a profitable real estate investment business.

Here’s our step-by-step guide on how to find top-performing long term and short term rental properties:

Step 1: Find the Best Market for Real Estate Investing

The first step in buying a top investment property in 2023 is identifying the best short term rental markets or long term rental markets, depending on your preferred strategy. It includes the state, the city, and the neighborhood, as real estate is very regional. The process usually requires extensive research and can take several months.

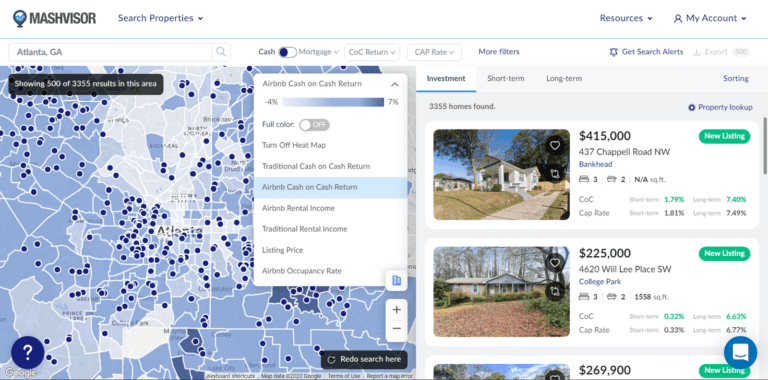

With the help of the Mashvisor real estate investing app, you can locate the best places for investment properties in a few minutes. For state- and city-level research, you can check out the Mashvisor real estate blog. There, you will find up-to-date rankings on the best states to buy investment property, as well as the best cities.

Then, you can use the Mashvisor real estate heatmap tool to search for the top neighborhoods for long term or short term rental properties. The available filters include the following:

Mashvisor’s real estate heatmap tool allows investors to search for the top neighborhoods for long term or short term rental properties using different filters.

After you locate a few potentially good neighborhoods, you can make use of the Mashvisor neighborhood analysis to deepen your real estate market analysis. It will give you access to all the metrics and numbers that you need in order to decide if a neighborhood is a good choice for investing in rental properties.

Importantly, all real estate and rental data involved in Mashvisor’s analysis comes from reputable sources like the MLS, RentJungle, Redfin, Airbnb, and public records.

Related: What Is the Best Real Estate Investing App?

Step 2: Locate a Top Rental Property for Sale

The second step in finding an investment property is searching for available real estate listings. While you can use traditional methods like newspapers, networking, and driving for dollars, they’re not the most efficient way to locate good opportunities. Thanks to technology, there are now various websites and online marketplaces targeting real estate investors.

For example, you can use the Mashvisor investment property search engine to look for listings that match your exact requirements. They include both MLS listings and some off market properties, each with its own pros and cons from an investor’s point of view.

Through the available filters, you can focus your search on a specific market, budget, financing option, property type, rental income, and return on investment. After setting up these criteria, you will get immediate access to the properties that match your expectations.

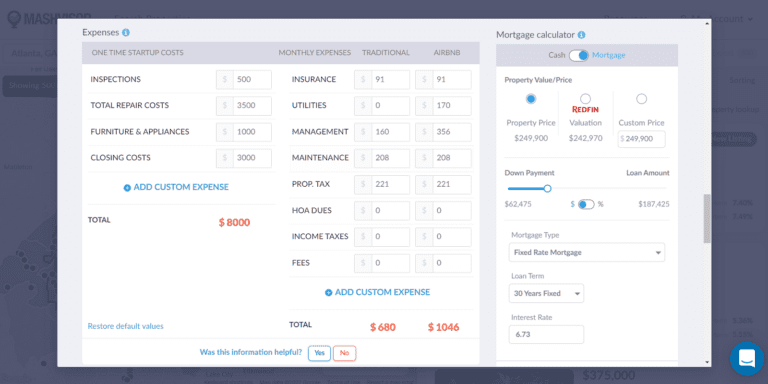

As soon as you see all available listings within your requirements, you can conduct detailed rental property analysis on them. The Mashvisor investment property calculator facilitates the said process. It provides a side-by-side comparison of the investment potential of a property when rented out on a long term or short term basis.

Related: Mashvisor: The #1 Investment Property Calculator for 2023

The analysis includes all numbers an investor needs to decide if it is a good opportunity, including:

- Listing price

- Startup costs

- Monthly rental income

- Recurring expenses

- Occupancy rate

- Cash flow

- Cash on cash return

- Cap rate

So, within a few minutes of online research, you can find potential investment properties for sale and confirm if they match your expectations.

Step 3: Figure Out the Best Loan for investment Property for You

The third step in buying the best investment property in 2023 is securing the top loan type. It is a rather personal decision, as what is best for one investor is not necessarily best for you. To tackle such an important decision, you should study carefully the available financing options and then evaluate your own financial situation. This way, you will know which loans you qualify for.

Once again, Mashvisor can help you. We’ve developed an investor-targeted mortgage calculator. While it is officially called a mortgage calculator, the tool can be adjusted to apply to different types of best loans for investment property.

In our rental property calculator, you can choose:

- Cash vs loan

- Property price

- Down payment as a dollar amount or a percentage

- Mortgage type

- Loan term

- Interest rate

All numbers are initially preset to reflect the most common situation in the real estate market. However, you can adjust all these variables to find out the best options for you and your investment property. All changes you make will be reflected in the detailed investment property analysis to show how they affect your ROI.

With Mashvsisor’s mortgage calculator, you can adjust the different loan metrics, such as down payment, mortgage type, loan term, and interest rate, according to the different types of best loans for investment property.

Step 4: Hire an Agent

The final step in purchasing the best possible income property in 2023 is working with an agent. Unless you have significant experience in negotiating and closing real estate deals, we strongly recommend hiring a real estate agent. They are professionals who can really help you optimize your investment results.

Moreover, as a buyer, in the US housing market, you don’t pay the agent fees as those are covered by the seller. In other words, you have nothing to lose from working with an agent, and you can gain a lot.

To start searching for the best investment properties to buy with the best loans, sign up for a 7-day free trial of Mashvisor.

Getting Started With the Best Loans for Investment Property in 2023

According to US housing market predictions, 2023 promises to be a great year for real estate investments. However, the success of your rental property business depends to a large extent on the financing method that you use. So, it’s crucial to choose from the best loans for investment property tailored to your particular situation.

In the vast majority of cases, real estate investors go for one of the following options:

- Conventional mortgage loans

- FHA loans

- VA loans

- Hard money loans

- Private money loans

- HELOCs

- Crowdfunding

Since rental property investing is so competitive, it’s crucial to find the best market, the best investment property, and the best loan quickly and confidently. To achieve it, you can use the Mashvisor platform to conduct nationwide rental market research, as well as individual investment property search and analysis.

You can turn months of real estate research and analysis into 15 minutes. All the while, you will have access to reliable data that has been analyzed to reflect the exact potential of the property you’re interested in, based on the performance or rental comps.

To unleash the full potential of Mashvisor to facilitate your real estate investments in 2023, schedule a free demo with our product specialists.