Zoom Video (NASDAQ: ZM) has gone from an obscure but easy-to-use video communications platform to becoming a verb synonymous with video conferencing and remote engagement driven by the COVID-19 pandemic. Zoom Video was one of the major benefactors of the pandemic that helped usher in the “new normal” of hybrid work in a post-pandemic world. While other video calling tools were available, Zoom’s incredibly easy interface brought video conferencing to the mainstream masses. The Company’s growth has since peaked as normalization continues to set in. The question is where the baseline is for Zoom and what catalysts can help it speed growth back up. The Company compete with many teleconferencing and business collaboration software companies like Adobe (NASDAQ: ADBE), Microsoft Teams (NASDAQ: MSFT), Salesforce (NASDAQ: CRM), Google Workspace (NASDAQ: GOOG), Cisco Webex Meetings (NASDAQ: CSCO) and even Verizon (NYSE: VZ) with its BlueJeans Meetings app. The Company wants to become a unified communication platform with the addition of email and calendar functions. It has also partnered with AMC Entertainment (NYSE: AMC) to turn some locations into Zoom meeting rooms

MarketBeat.com – MarketBeat

Growth Continues to Slow

On Nov. 21, 2022, Zoom Video released its third-quarter fiscal 2023 results for the quarter ending October 2022. The Company reported earnings-per-share (EPS) profit of $1.07 beating consensus analyst estimates for a profit of $0.84 by $0.23. Revenues rose 4.9% year-over-year (YoY) to $1.1 billion, matching consensus analyst estimates for $1.1 billion. $100,000 annual run rate (ARR) customers rose 31% to 3,286. Enterprise customers rose 14% YoY to 209,300. Enterprise revenue rose 20% YoY to $614 million. Online average monthly churn was 3.1% down 60 basis points from same period last year. Zoom Video ended the quarter with $5.2 billion in cash and cash equivalents and marketable securities. Zoom Video CEO Eric Yuan commented, “Our customers are increasingly looking to Zoom to help them enable flexible work environments and empower authentic connections and collaboration. Proactively addressing these needs with Zoom’s expanding platform continues to be our focus in this dynamic environment.”

Lump of Coal Guidance

Zoom Video issued downside guidance for fiscal Q4 2023 with EPS between $0.75 to $0.78 versus $0.82 consensus analyst estimates. Fiscal Q4 2023 revenues are expected to come in between $1.095 billion and $1.105 billion versus $1.12 billion. Incidentally, constant currency revenues are expected between $1.12 billion to $1.13 billion. Total fiscal 2023 revenues are expected between $4.370 billion to $4.380 billion and $4.42 billion to $4.452 billion in constant currency. Non-GAAP EPS for full-year fiscal 2023 is expected between $3.91 to $3.94 with 304 million weight average shares outstanding.

Analysts Cut Price Targets

Piper Sandler lefts its Neutral rating unchanged but cut its target price to $77 from $84 per share. Analyst James Fish was underwhelmed by its Q4 lump of coal outlook and concerned for the declining total customer base as the rate of new business continues to decelerate. Baird kept its Outperform rating but slashed the price target for Zoom shares to $95 from $100 per share. Analyst William Power felt the Q3 2022 results were solid, but its outlook remained mixed due to currency headwinds are weaker deferred revenues. Zoom remains a top holding at 8.31% in the Ark Innovation ETF (NYSEARCA: ARKK) operated by famed fund manager Cathie Wood.

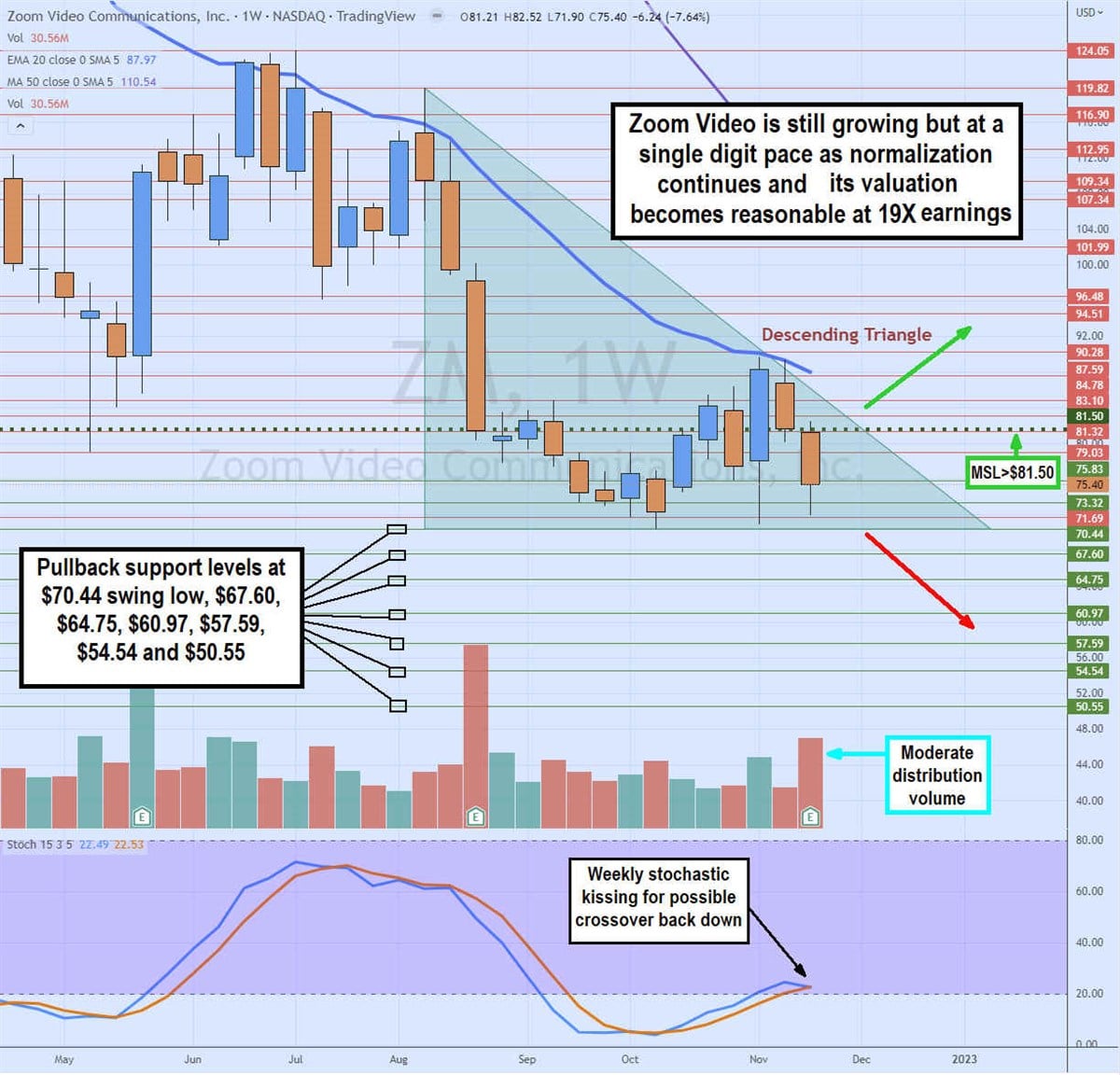

Weekly Descending Triangle Risk

The weekly candlestick chart illustrates the potential for a descending triangle breakdown as it makes lower highs against a flat low at $70.44. Shares continue to reject off the falling weekly 20-period exponential moving average (EMA) now at $87.97. The Q3 2022 earnings reaction further accelerated the selling towards the $70.44 low area before a coil attempt failed to trigger the weekly market structure low (MSL) buy trigger above $81.50. Distribution volume rose upon the earnings release but was moderate compared to nearly double the volume on its Q2 2022 earnings sell-off. The weekly stochastic bounce through the 20-band stalled on the selling pressure setting it up for a potential crossover back down as shares near the flat lower trendline of the weekly triangle. As the channel between the falling upper trendline and flat trendline gets tighter towards the apex, shares will either breakout by triggering the weekly MSL or finally breakdown through the swing lows. This should resolve by the end of the year. Pullback support levels to watch sit at the $70.44 swing low, $67.60, $64.75, $60.97, %57.59, $54.54, and the $50.55.