[ad_1]

Mobile payment apps can be a convenient way to send and receive money using your smartphone or smartwatch. Paying for items this way has never been easier, thanks to the availability of numerous mobile payment apps, better payment terminal infrastructure, and wider support for Bluetooth/near-field communication (NFC) contactless credit cards by American issuers. The coronavirus pandemic has also helped to make contactless “everything” more compelling, so being able to use our smartphones or smartwatches for mobile banking and payments is as appealing as ever.

Over the course of several weeks, we tested out five different mobile payment apps: Apple Pay, Google Pay, Samsung Pay, Venmo (by PayPal) and Cash App (by Block, formerly Square). We tested Apple Pay and Samsung Pay on just their own devices and tested Google Pay, Venmo and Cash App on both Android and iOS.

The apps work across a variety of web browsers (with the exception of Samsung) and watches. We tested the apps on an Apple Watch and a Samsung Galaxy Watch. We tested each of them with the following in mind: ease of installation, ease of setup, features, security, fees and customer support. As our testing concluded, two clear winners emerged: Apple Pay and Google Pay.

Best mobile payment app overall

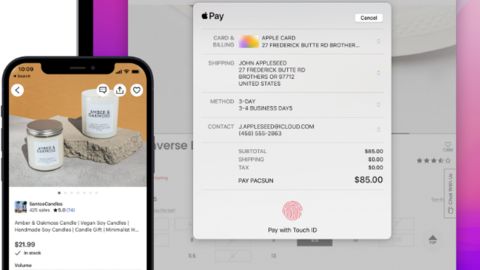

While Apple Pay only works on iOS devices, its user interface is uncluttered and simple to use. The app also offers robust security and authentication for all your purchases, and offers 2% cash back on P2P payments.

While Apple Pay only works for its own devices, it is available in numerous countries, and its elegant and simple user interface (UI) and design make it a standout. Peer-to-peer (P2P) payments are only available in the United States. On your iOS device, you need to set up Face ID, Touch ID or a passcode. On your Apple Watch, you need to set up a passcode. You also need to be 13 years old or older.

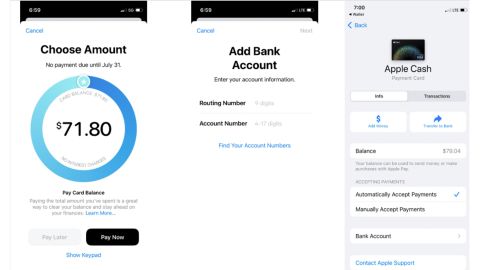

If you want to make a P2P payment, then you’ll need to send an Apple Message, which means you need to know your recipient’s phone number or email address. One nice feature is that all transactions generate 2% cash back. If you have an Apple Watch, then you need to connect your cards and bank accounts specifically on the watch for use in payments.

Runner up to the best mobile payment app overall

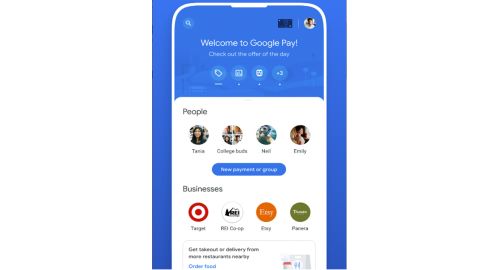

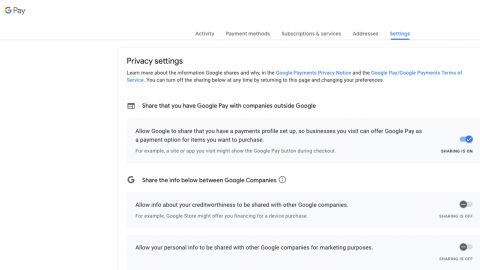

Google Pay offers strong privacy options that let you opt out of sharing data with outside vendors or among various Google companies. It works with a variety of credit cards and doesn’t charge any fees.

Google Pay has different lists of countries and regions in which it is available depending on the transaction type intended. Google Pay works across Android and iOS and is also designed to be capable in your browser. There aren’t any fees and immediate transfers are from debit cards only.

Since Google Pay also works through browser cookies, it doesn’t require your phone to complete any online transactions. But, since it works through your Google account, you will have to exchange emails to set up the payment. Also, you will need a personal account (Pay won’t work with workspace or enterprise accounts).

There are three different use cases for these apps (which we tested) that we will explain, as well as three other use cases that we will mention (even though we didn’t test these).

The first use case we tested is making P2P cash payments. Two examples of this are splitting a restaurant check and sending gift money to family and friends. Consumers are increasingly using these apps according to a recent survey by Lending Tree. The survey showed that 84% of the 1,200 respondents (all U.S. consumers) have used at least one mobile payment app in the past year. Samsung Pay doesn’t support this mode but the other apps do.

Some of the apps let you set up pools of funds, like a miniature version of GoFundMe to which your friends can send you contributions. There are several ways to identify your recipient: by their phone number and email address, or by their username (Block and Venmo support this) and, in some cases, by using a personal QR code (Block and Venmo are focused on this use case).

The second use case we tested is paying for retail purchases instead of directly using a credit card or debit card. When the time comes to pay at a physical store, you hold your smartphone (or smartwatch) close to the payment terminal and it should read the appropriate card. This can be useful if you load multiple cards on the payment app, so you don’t have to cart around an overstuffed wallet with physical cards. It is also more secure because most of the payment apps create and then send a one-time token instead of your actual card number for each transaction. (Apple Pay and Google Pay are focused on this use case, although both also support P2P payments, too.)

The third use case we tested is using them whenever you are shopping online. The Apple Pay and Google Pay apps can be used here. You can also store your card details in the various desktop browsers so that they can be auto-filled when you are at the checkout screen of your favorite retailer.

So, now for the other use cases we didn’t test but are worth mentioning. Each of the payment apps has moved beyond these three core situations and now offer three other use cases: 1) a complex series of their own branded credit cards and debit cards, 2) support for Bitcoin purchases and other money-related features, and 3) cash-back offers. Again, we didn’t test these last three use cases; however, it is worth paying attention to at least the one about cash-back offers because those can really add up over time.

Should you be worried about scammers when using mobile payment apps? Yes — the same Lending Tree survey we cited earlier found that 15% of the respondents have been victims of scams. And the survey also mentioned that, though P2P services are growing, they’re not FDIC insured. The survey found that “62% of consumers knew FDIC doesn’t insure P2P balances. However, 49% of those who keep a balance wrongly believe their money is protected.”

If you intend to use any of these mobile payment apps on a regular basis, then you’ll want to follow these 6 steps:

- Step 1: Protect your payment app with the strongest authentication you can use. You should use your face or fingerprint to open the app and to send money.

- Step 2: Enable multi-factor authentication (MFA) as another way to protect your log-in. Even if you don’t plan on using any of the browser versions, you still want to protect this access method.

- Step 3: Set up app notifications of any transactions. That way, you will confirm what is going on.

- Step 4: Pay attention to what you are doing when using any app. The opportunity to make a mistake, especially while multitasking and the fact that you can’t cancel any completed transaction, can mean trouble.

- Step 5: Don’t send money to strangers. Realize that, unlike bank transactions, there is no built-in fraud prevention when using mobile payment apps. Once you send the money, it is gone for good. So triple-check the details before clicking Send.

- Step 6: If you are buying physical goods, then use your browser and the stored card feature in your browser.

- Tip: The US Federal Trade Commission (FTC) has more tips on how to avoid a scam when using mobile payment apps and Fraud.org, a project of the National Consumers League (NCL), offers advice on how to avoid falling victim to these types of scams as well.

During our pretesting research, we found there are more than 20 different payment apps available, including apps from retailers like Starbucks and apps from Mastercard and Visa. We selected our five payment apps to test based on desired features, security options and user reviews. We tested each of them with the following criteria in mind: ease of installation, ease of setup, features, security, customer support and fees.

To begin our testing, we installed the apps on one or both types of smartphones (if supported) and on an Apple Watch and Samsung Galaxy Watch.

Next, we connected to various bank accounts and credit cards and debit cards, using them for retail purchases and P2P payments. We also tried each app when it was available for online retail purchases. We tested each app’s MFA support and other security features. We tested each app’s ability to notify you of payment transactions, and to block someone else from initiating a payment without your biometric data or other factors to approve it.

Then we noted that the workflows for the payment apps were similar across the lot. We first ensured we were downloading the correct payment app from the legit app store. This is important and you should take care here. We then connected the app to either our phone number or email address (most apps want both), and then typed in a bank account or card that was to be the source and destination of our funds.

This was the moment of truth, because not every payment app supported every bank card (and we didn’t find out until we got to this step). Apple Pay and Google Pay worked with more of our credit cards than the others did, but your experience could be different.

After that, we set up our app’s security with our face or fingerprint to protect our transactions. It sounds more complicated than it actually was. After a flurry of confirmation emails and texts, we were ready to go shopping or send our friends some money.

One of the big advantages of these apps is that you forgo the need to carry cash and you can pay someone on the spot. However, for all of these apps, our patience was rewarded. If we wanted to make a P2P payment and our recipient was willing to wait a few days, then there wasn’t any fee applied.

But if we wanted the payment to happen in a matter of minutes, then it cost us.

For example, all the apps were free to download. But when it came to fees, Apple charges 1.5% (with a minimum $0.25 and maximum $15 fee) and Venmo adds a 1% surcharge (with a maximum $10 fee). Square is free for all personal accounts but charges 2.75% for business users. Google Pay and Samsung Pay have no added fees.

Lastly, we also reviewed complaints collected by CardPaymentOptions.com for Apple Pay, Google Pay, Samsung Pay, Cash App and Venmo. And we tried out the various support options available for each service. All five apps had equivalent high scores on both. Cash App, Samsung Pay and Venmo all share data with third parties to track internal marketing. Apple Pay and Google Pay don’t do this, although they may use this data internally across their various properties.

During our testing, we used an Apple Watch and Samsung Galaxy Watch to gauge how easy it is to use a smartwatch versus a smartphone for mobile payments. So, is your smartwatch better to use than your phone for payments? No, we don’t think so.

We found the watch movements needed to get close enough to the payment terminal to make a connection were more cumbersome than they were when we used our phone. And the usability factors to set up the account on the watches are sub-par. If you use your watch for other apps, then great, but don’t rush out and get a watch just for payments.

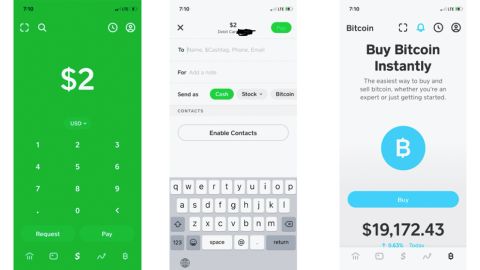

Free at Cash App

With Cash App, which is owned by Block (formerly Square, Inc.), you set up a username that your friends can use to find you when sending or demanding funds. You do not need to know their phone number or email address. Cash App is limited to debit cards only for direct access. It also uses Plaid for connecting to your bank account, which we think adds another layer of security issues.

There are also various transfer limits, too, for unidentified users (e.g., sending $250 over per week or receiving $1,000 over a month). You can set up recurring deposits, direct deposits, make bank transfers and even file your taxes.

There is a 3% fee if you are moving funds with a credit card. You can also instantly purchase or sell Bitcoin from the app. Cash App also works with the Lightning network to pay anyone with these cryptocurrencies.

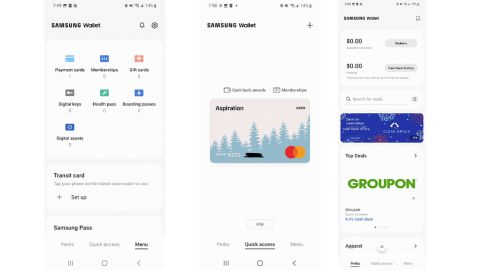

Free at Samsung

Samsung Pay works in several countries, but it is only available on Samsung smartphones and smartwatches. It is basically a stripped-down version of Google Pay, using the same banking backends. It requires your mobile number to complete its setup, and in our testing we found it didn’t support several of the debit cards we owned. It also doesn’t support any P2P payments: you’ll need to use the separate Samsung Pay Cash app.

One advantage is that, while Apple Pay and Google Pay will only work with point-of-sale (POS) payment terminals equipped with NFC technology, Samsung Pay (from the phone, not from the watch) works at magnetic card terminals — those few that are left and haven’t been upgraded — as well.

We had trouble getting the Samsung Pay app to work with the Samsung Galaxy Watch (like Apple Pay, you have to separately install each card to use on the watch), and needed to install and re-install various Samsung apps. We recommend using Google Pay instead.

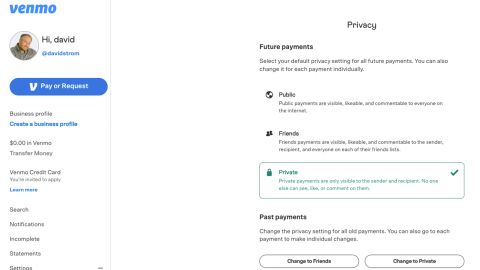

Free at Venmo

Venmo, which is only available in the United States, was simple to set up and get connected to our bank card. Like Cash App, you can send money using a username, which obviates the need to know a friend’s phone number or email address. One drawback to Venmo is that all of your friends’ transactions are made public by default, so anyone can see them in its public feed. This means the first thing you need to do when using this service is turn these settings to Private.

Venmo also supports Bitcoin, Bitcoin Cash, Ethereum or Litecoin currency transactions. If you are sending funds from a credit card and can’t wait, then there is a 3% fee. Funds sent from your bank account are free if you can wait a few days. Fees are clearly described on their Resources page and there are fees for unverified users when sending more than $300 per week.

Venmo’s browser client mirrors the UI for its phone app screens, which is useful for reviewing its numerous configuration settings. But it could do a better job explaining its security protocols.

Read more from CNN Underscored’s hands-on testing and tech coverage:

[ad_2]